The first thing you will notice is the executive change from the previous call:

Mark H. Henninger - Intel Corp.

Brian M. Krzanich - Intel Corp.

Robert Holmes Swan - Intel Corp.

Mark H. Henninger - Intel Corp.

Robert Holmes Swan - Intel Corp.

Venkata S. M. Renduchintala - Intel Corp.

Navin Shenoy - Intel Corp.

Navin is VP/GM of the Data Center group and Murthy (Venkata) has a handful titles so nobody really knows what he actually does. Intel posted some impressive numbers but the call itself was typical Intel doublespeak:

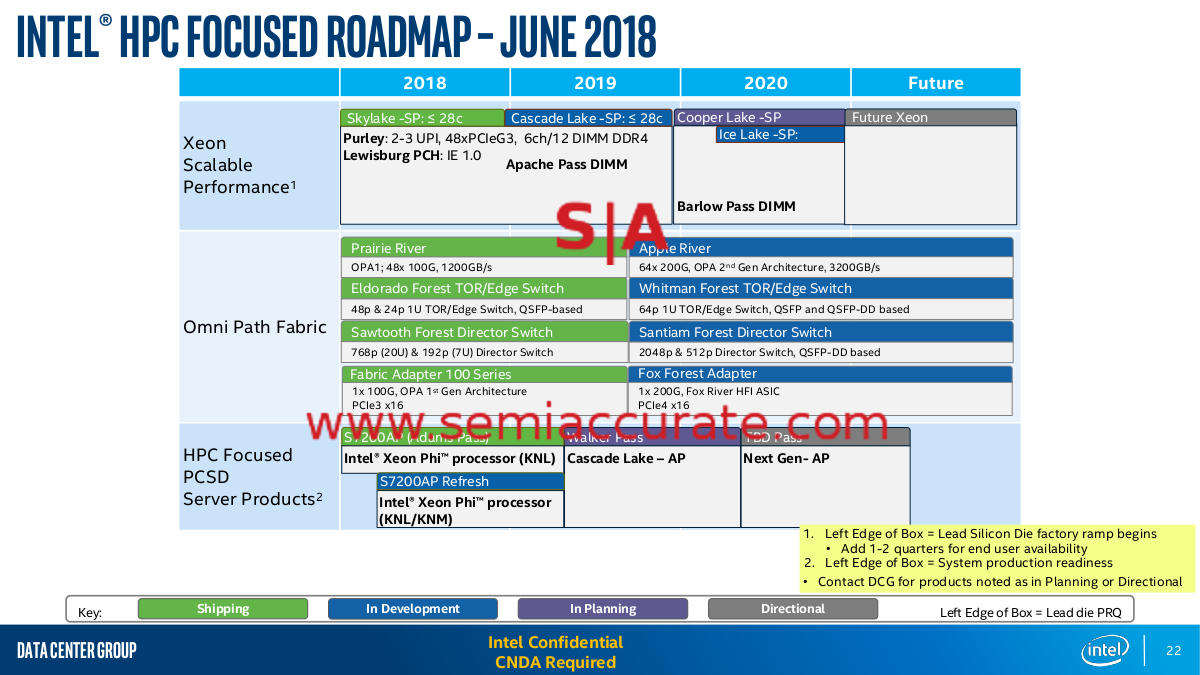

10nm Question:

Venkata S. M. Renduchintala - Intel Corp.

Hi, this is Murthy. I'll take that one. We continue to make progress on 10-nanometer. Yields are improving consistent with the timelines we shared in April. And yes, you're quite right. The systems on shelves that we expect in holiday 2019 will be client systems, with data center products to follow shortly after.

10nm question:

Venkata S. M. Renduchintala - Intel Corp.

So let me take that. I think as we look at what we need to do in 10-nanometers, again, let me replay some of the data we shared on our April call. Recall that 10-nanometers strive for a very aggressive density improvement target beyond 14-nanometers, almost 2.7x scaling. And really, the challenges that we're facing on 10-nanometers is delivering on all the revolutionary modules that ultimately deliver on that program. And while there's risk and a degree of delay in our timeline on that, we're very pleased with the resiliency of our 14-nanometer roadmap, where in the last few years we've delivered in excess of 70% product performance improvement as we've moved through our 14-nanometer generation of products.

So as we look at 2019 across both the client and data center space, we feel very good about the product competitiveness of our 14-nanometer program, and that to some degree is factoring into our timing on 10-nanometer and launching 10-nanometer at a point in time where we believe the yields are at a level that make it prime for volume production. So 14-nanometer I think through the rest of this year and through 2019 continues, we believe, to drive product leadership across all our portfolio in client and server.

7nm Question:

Venkata S. M. Renduchintala - Intel Corp.

Sure. Blayne, so 7-nanometer is very much R&D in deep progress, and we're making good progress on that development. We're not giving a direct timeline right now. But we've also made some fairly judicious choices in defining 7-nanometer, learning from our 10-nanometer experiences. And we're focusing on an optimum balance point between density, power and performance, and schedule predictability. So I think what you'll see is a more balanced approach across those three vectors.

So we're still going to drive density but balancing that with a continued focus on driving transistor performance at the same time, which is highly valued as ASP drivers both in our client and server businesses. And we're really also focusing on being much more precise in our ability to launch. So those are the key learnings that are coming out of 10-nanometer as we go into 7-nanometer. And as we monitor progress on 7-nanometer just as closely as we are on 10-nanometer, I feel those lessons are being well absorbed into our progress, and we're lining up to support our product plans as our roadmap dictates.

10nm Question:

Venkata S. M. Renduchintala - Intel Corp.

In general, we're going to see a much shorter ramp period between our products going forward in client and server. So yes, I think it's a good observation that as we talk about client systems on shelf by the second half of 2018, you shouldn't expect too much of a delay before you see data center products coming out.

So much closer proximity, albeit slightly delayed than we expected on 10-nanometer, and then you should see that pretty much improve to almost parity of launches as we get into later technologies. So the traditional model of server following rather lengthily after client is probably going to become more sequential going forward.

"Client systems on the shelf by the second half of 2018" ?!?!?

10nm Question:

Venkata S. M. Renduchintala - Intel Corp.

I just wanted to add to Bob's perspective. The way I look at our roadmap, what we're really focused on is delivering product leadership generation after generation, and that's the system level. And while processes are a very important part of that recipe, so are the other ingredients as well, such as product architecture, silicon design, and packaging.

And to Bob's point, as we look towards our roadmap, gross margin maximization is going to come from delivering excellence that drives performance, and therefore we're taking a very balanced view in all the ingredients that go into that. So you should expect in our roadmap going forward a much longer overlap between generations of technology as we try and make sure that, along with process, we add the other ingredients of technology leadership that will become more and more apparent.

If this was a CEO tryout I would say that Murthy passed the Intel doublespeak test with flying colors. And last but not least the fitting sendoff of BK who the Intel BoD completely threw under the bus:

Robert Holmes Swan - Intel Corp.

Personally and on behalf of Intel's 100,000-plus employees, I'd like to thank Brian [Krzanich] for his many contributions to the company over his 35-year career. The investments he made set us on a course for transformation. Even more importantly, he developed the right strategy and leadership team to carry that transformation forward while we conduct the CEO search. Our financial results in the second quarter show we're doing just that.

Mark H. Henninger - Intel Corp.

Brian M. Krzanich - Intel Corp.

Robert Holmes Swan - Intel Corp.

Mark H. Henninger - Intel Corp.

Robert Holmes Swan - Intel Corp.

Venkata S. M. Renduchintala - Intel Corp.

Navin Shenoy - Intel Corp.

Navin is VP/GM of the Data Center group and Murthy (Venkata) has a handful titles so nobody really knows what he actually does. Intel posted some impressive numbers but the call itself was typical Intel doublespeak:

- Record second-quarter revenue was $17.0 billion, up 15 percent year-over-year (YoY); data-centricbusinesses* grew 26 percent and PC-centric revenue grew 6 percent.

- GAAP earnings-per-share (EPS) of $1.05 rose 82 percent YoY; non-GAAP EPS of $1.04 was up 44 percent.

- Year-to-date, generated $13.7 billion in cash from operations, $6.3 billion of free cash flow and returned $8.6billion to shareholders (dividends of $2.8 billion and share repurchases of $5.8 billion).

- Raising full-year revenue outlook to approximately $69.5 billion, GAAP EPS outlook to approximately $4.10 andnon-GAAP EPS of $4.15; up $2.0 billion, $0.31 and $0.30 from April guidance, respectively.

10nm Question:

Venkata S. M. Renduchintala - Intel Corp.

Hi, this is Murthy. I'll take that one. We continue to make progress on 10-nanometer. Yields are improving consistent with the timelines we shared in April. And yes, you're quite right. The systems on shelves that we expect in holiday 2019 will be client systems, with data center products to follow shortly after.

10nm question:

Venkata S. M. Renduchintala - Intel Corp.

So let me take that. I think as we look at what we need to do in 10-nanometers, again, let me replay some of the data we shared on our April call. Recall that 10-nanometers strive for a very aggressive density improvement target beyond 14-nanometers, almost 2.7x scaling. And really, the challenges that we're facing on 10-nanometers is delivering on all the revolutionary modules that ultimately deliver on that program. And while there's risk and a degree of delay in our timeline on that, we're very pleased with the resiliency of our 14-nanometer roadmap, where in the last few years we've delivered in excess of 70% product performance improvement as we've moved through our 14-nanometer generation of products.

So as we look at 2019 across both the client and data center space, we feel very good about the product competitiveness of our 14-nanometer program, and that to some degree is factoring into our timing on 10-nanometer and launching 10-nanometer at a point in time where we believe the yields are at a level that make it prime for volume production. So 14-nanometer I think through the rest of this year and through 2019 continues, we believe, to drive product leadership across all our portfolio in client and server.

7nm Question:

Venkata S. M. Renduchintala - Intel Corp.

Sure. Blayne, so 7-nanometer is very much R&D in deep progress, and we're making good progress on that development. We're not giving a direct timeline right now. But we've also made some fairly judicious choices in defining 7-nanometer, learning from our 10-nanometer experiences. And we're focusing on an optimum balance point between density, power and performance, and schedule predictability. So I think what you'll see is a more balanced approach across those three vectors.

So we're still going to drive density but balancing that with a continued focus on driving transistor performance at the same time, which is highly valued as ASP drivers both in our client and server businesses. And we're really also focusing on being much more precise in our ability to launch. So those are the key learnings that are coming out of 10-nanometer as we go into 7-nanometer. And as we monitor progress on 7-nanometer just as closely as we are on 10-nanometer, I feel those lessons are being well absorbed into our progress, and we're lining up to support our product plans as our roadmap dictates.

10nm Question:

Venkata S. M. Renduchintala - Intel Corp.

In general, we're going to see a much shorter ramp period between our products going forward in client and server. So yes, I think it's a good observation that as we talk about client systems on shelf by the second half of 2018, you shouldn't expect too much of a delay before you see data center products coming out.

So much closer proximity, albeit slightly delayed than we expected on 10-nanometer, and then you should see that pretty much improve to almost parity of launches as we get into later technologies. So the traditional model of server following rather lengthily after client is probably going to become more sequential going forward.

"Client systems on the shelf by the second half of 2018" ?!?!?

10nm Question:

Venkata S. M. Renduchintala - Intel Corp.

I just wanted to add to Bob's perspective. The way I look at our roadmap, what we're really focused on is delivering product leadership generation after generation, and that's the system level. And while processes are a very important part of that recipe, so are the other ingredients as well, such as product architecture, silicon design, and packaging.

And to Bob's point, as we look towards our roadmap, gross margin maximization is going to come from delivering excellence that drives performance, and therefore we're taking a very balanced view in all the ingredients that go into that. So you should expect in our roadmap going forward a much longer overlap between generations of technology as we try and make sure that, along with process, we add the other ingredients of technology leadership that will become more and more apparent.

If this was a CEO tryout I would say that Murthy passed the Intel doublespeak test with flying colors. And last but not least the fitting sendoff of BK who the Intel BoD completely threw under the bus:

Robert Holmes Swan - Intel Corp.

Personally and on behalf of Intel's 100,000-plus employees, I'd like to thank Brian [Krzanich] for his many contributions to the company over his 35-year career. The investments he made set us on a course for transformation. Even more importantly, he developed the right strategy and leadership team to carry that transformation forward while we conduct the CEO search. Our financial results in the second quarter show we're doing just that.

Last edited: