My opinion: you might compare orange to apple. Specialty technology might work on 150/200mm or mature 300mm wafer fab. The ASP could be much lower than leading edge technology, but the margin will be higher. It should be higher than the current margin of intel 7.

I agree with you that Tower's real ASP may be much lower. I attempted to use public available data to show Tower's ASP is not in the same camp of Intel. Only Intel and Tower Semiconductor can answer the question about Tower's actual ASP and the number of wafer/chip it produced. Hope some analysts will ask Tower Semi tomorrow during their earnings conference call.

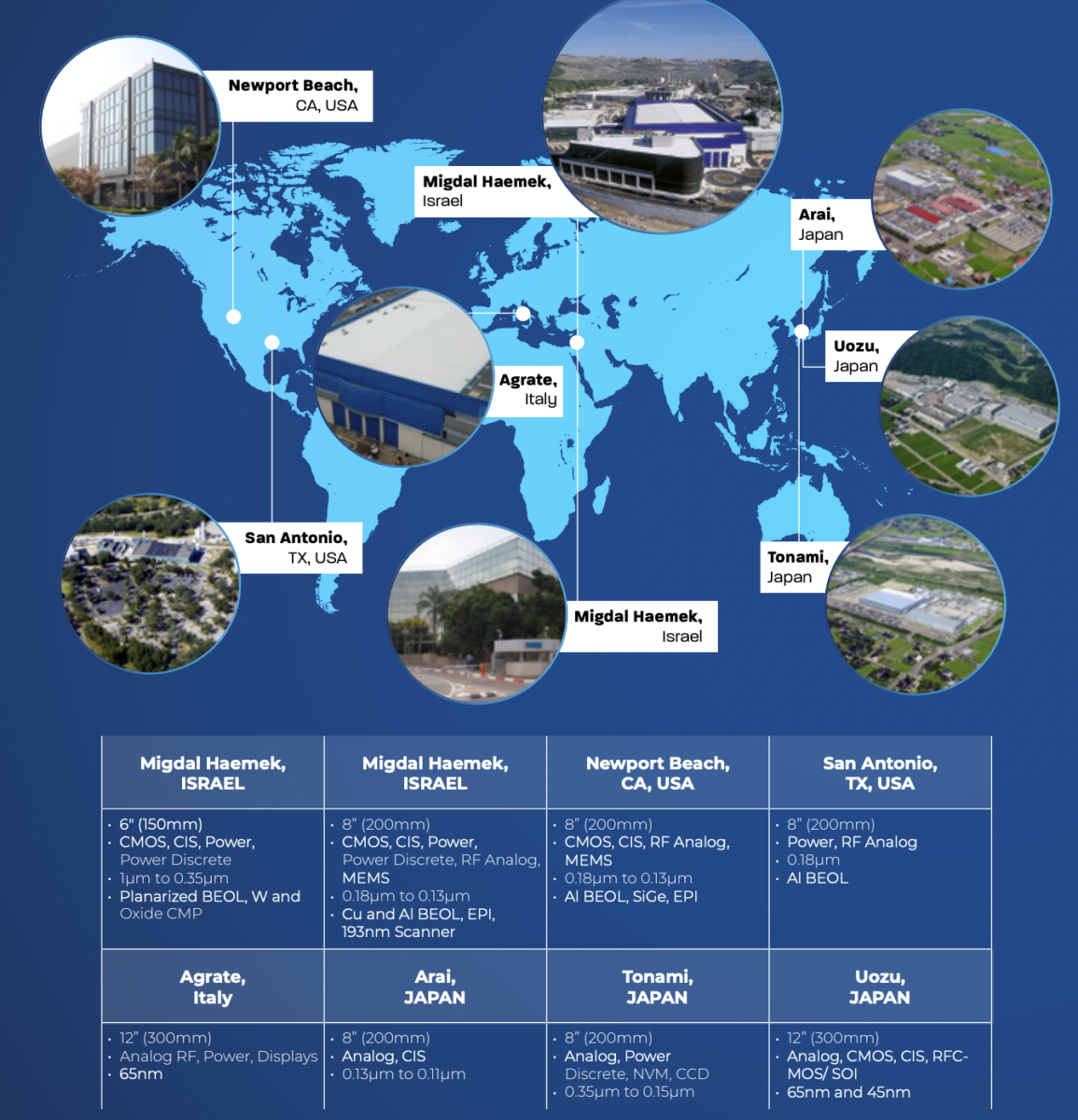

I don't know what Intel 7 current profit margin is and I don't think Intel will reveal such detail information down to process node level. On the other hand we do know how Tower Semiconductor performed in the past. Using their third quarter 2021 financial data as an example (Tower Semiconductor will release 2021 full year result tomorrow February 17, 2022) :

Tower Semiconductor Third Quarter of 2021 Results:

Revenue: $387 million

Gross profit: $85 million

Operating profit: $44 million

Net profit: $39 million

TSEM Gross profit margin: 21.96% (Intel 55.4% 2021)

TSEM Operating profit margin: 11.37% (Intel 24.6% 2021)

TSEM Net profit margin: 10.08% (Intel 25.19% 2021)

Tower Semiconductor (TSEM) is not a startup and has been doing business in the mature/specialty field for many years. I think many financial analysts treat buying TSEM as a "What You See Is What You Get" case. With such big difference in profitability, they are asking if TSEM a good fit for Intel's business model.

Everything in Intel from R&D, manufacturing, market and product selection, employee compensation, pricing, financial operations to dividends are built on the foundation of high volume, high price, and high profit margin business model.

Is this $5.4 billion acquisition worth it?