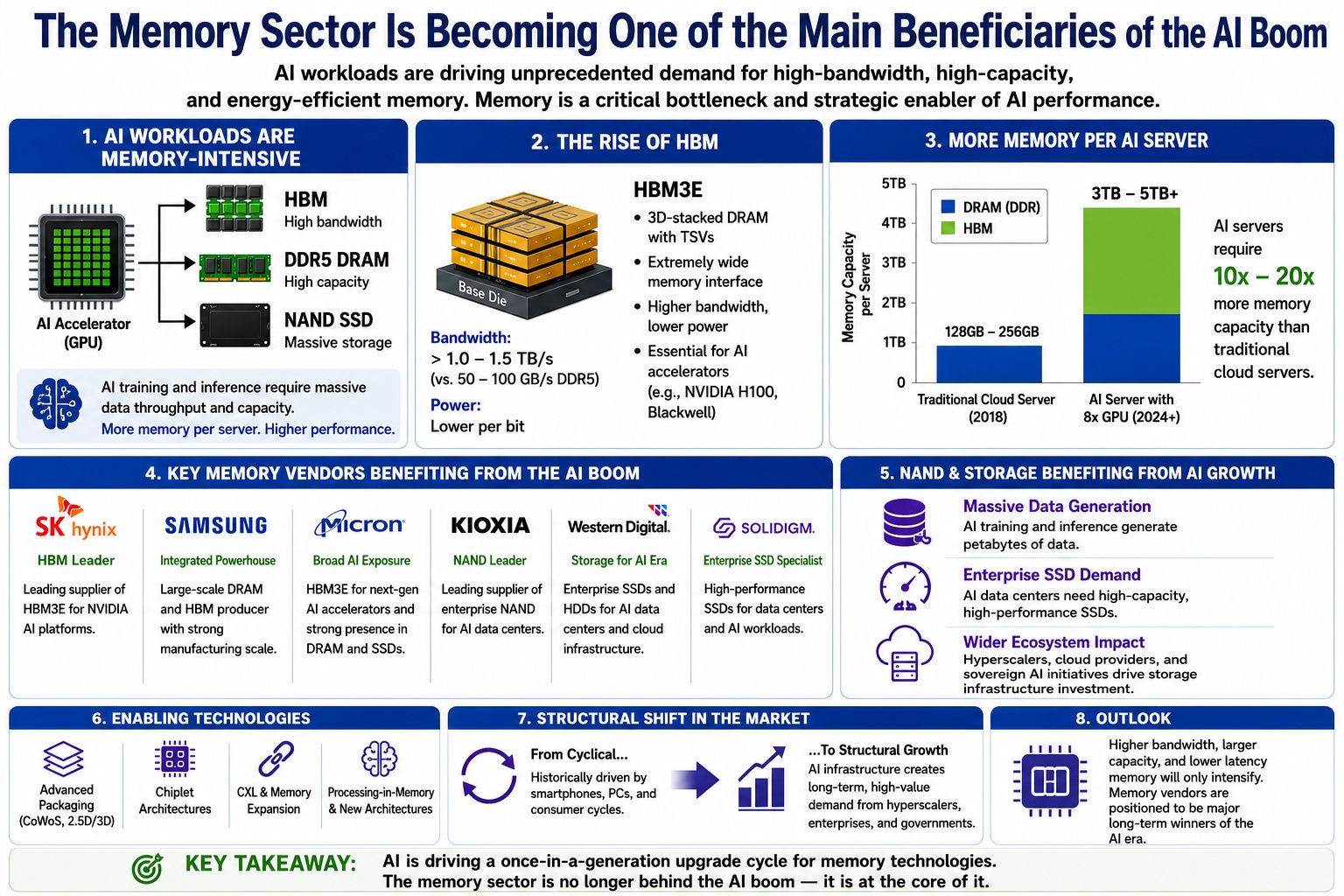

The explosive growth of artificial intelligence is transforming the semiconductor industry, and nowhere is this more evident than in the memory sector. AI training and inference workloads are fundamentally memory-intensive, driving unprecedented demand for advanced DRAM architectures, High Bandwidth Memory (HBM), and enterprise NAND storage. While GPUs from NVIDIA dominate headlines, the reality is that AI accelerators cannot function efficiently without massive amounts of high-performance memory tightly integrated into the compute architecture. As a result, memory vendors are emerging as some of the biggest long-term beneficiaries of the AI boom.

At the center of this transformation is HBM, a 3D-stacked DRAM technology that delivers significantly higher bandwidth and lower power consumption than conventional DDR memory. HBM uses through-silicon vias (TSVs) and advanced packaging techniques to vertically stack DRAM dies, enabling memory bandwidth measured in terabytes per second. AI accelerators such as NVIDIA’s H100 and upcoming Blackwell platforms depend heavily on HBM3 and HBM3E to feed data into thousands of parallel GPU cores during large language model (LLM) training.

This trend has dramatically altered the competitive dynamics of the memory market. SK hynix has emerged as the dominant supplier of HBM, reportedly securing a leading share of NVIDIA’s HBM3 and HBM3E supply chain. The company’s early investment in TSV technology, advanced packaging, and thermal management gave it a critical advantage as AI demand accelerated. SK hynix is now ramping HBM3E production aggressively and is expected to remain a key supplier for next-generation AI systems.

Samsung Electronics, the world’s largest memory manufacturer, is also investing heavily in HBM capacity and advanced packaging technologies. Samsung’s integrated semiconductor model—including logic, foundry, packaging, and memory—positions the company to compete aggressively in AI infrastructure. Although Samsung initially lagged behind SK hynix in HBM qualification for certain AI platforms, it remains a major long-term player due to its scale, process technology leadership, and ability to rapidly expand production.

Micron Technology has become another major AI beneficiary. Historically viewed as more cyclical and PC-dependent, Micron is now leveraging its advanced DRAM portfolio and HBM roadmap to gain exposure to hyperscale AI deployments. The company’s HBM3E products are being designed into next-generation AI accelerators, and management has repeatedly stated that HBM demand exceeds supply well into future production cycles. Micron’s strong position in enterprise DRAM and data center SSDs also gives it broad leverage to AI infrastructure spending.

AI workloads are increasing memory content per server at an extraordinary rate. Traditional cloud servers typically required several hundred gigabytes of DRAM, but AI servers equipped with multiple GPUs may contain several terabytes of high-bandwidth memory and DDR5 DRAM. A single NVIDIA HGX platform can contain eight GPUs connected with NVLink and supported by enormous pools of HBM. This architecture dramatically increases DRAM consumption per rack and boosts average selling prices for advanced memory products.

DDR5 adoption is also accelerating due to AI server deployments. Compared to DDR4, DDR5 provides higher bandwidth, improved power efficiency, and greater module density, all essential for data center AI workloads. Vendors including Samsung, SK hynix, and Micron are benefiting from the transition as hyperscalers upgrade infrastructure to support generative AI services.

Beyond DRAM, NAND flash suppliers are also positioned to benefit from AI expansion. Generative AI requires massive datasets for model training and inference, driving demand for high-capacity enterprise SSDs. AI data centers rely on fast storage systems to move and manage petabytes of structured and unstructured data. Companies such as Kioxia, Western Digital, Samsung, Micron, and Solidigm are therefore seeing growing demand for enterprise NAND solutions optimized for hyperscale environments.

Another critical technology trend is advanced packaging. AI accelerators increasingly use chiplet architectures and heterogeneous integration, where memory must be tightly coupled to compute dies. This creates opportunities not only for memory vendors but also for packaging leaders such as TSMC, Amkor, and ASE. CoWoS packaging capacity at TSMC has become particularly important because it enables integration of HBM stacks alongside AI GPUs and accelerators.

The AI boom is also reducing some of the historical cyclicality of the memory market. In the past, DRAM and NAND demand depended heavily on smartphones and PCs, leading to severe oversupply cycles. AI infrastructure spending introduces a new structural demand driver tied to hyperscale cloud expansion, enterprise AI adoption, and sovereign AI initiatives. This shift may support stronger long-term pricing and higher capital investment across the memory ecosystem.

Looking ahead, next-generation memory technologies including HBM4, MRAM, CXL-attached memory expansion, and processing-in-memory architectures could further reshape the industry. AI models continue to scale exponentially, requiring ever-larger memory pools and faster interconnects. As compute performance increasingly becomes constrained by memory bandwidth and latency rather than raw processing power, memory vendors are moving from supporting players to strategic enablers of the AI era.

Bottom line: The AI revolution is becoming as much a memory story as a compute story. Companies that can deliver high-bandwidth, low-power, and tightly integrated memory solutions are likely to capture a disproportionate share of semiconductor industry growth over the next decade.

Also Read:

WEBINAR: Engineering Documentation is a Critical Source of Truth – Do You Know if it’s Accurate?

WEBINAR: Caspia’s AI Makes You a Security Verification Expert

What Winemakers and Chip Designers Have in Common

Share this post via:

Synopsys and Intel Foundry Enable System-Level Design on Intel 14A