The global semiconductor industry sits at the foundation of modern technology, powering everything from smartphones and cloud data centers to artificial intelligence, automobiles, and national defense systems. At the center of advanced chip manufacturing are three major players: TSMC, Samsung Foundry, and Intel Foundry. Each represents a distinct manufacturing model and strategic philosophy, and together they form a competitive landscape that is essential for innovation, resilience, and long-term industry health.

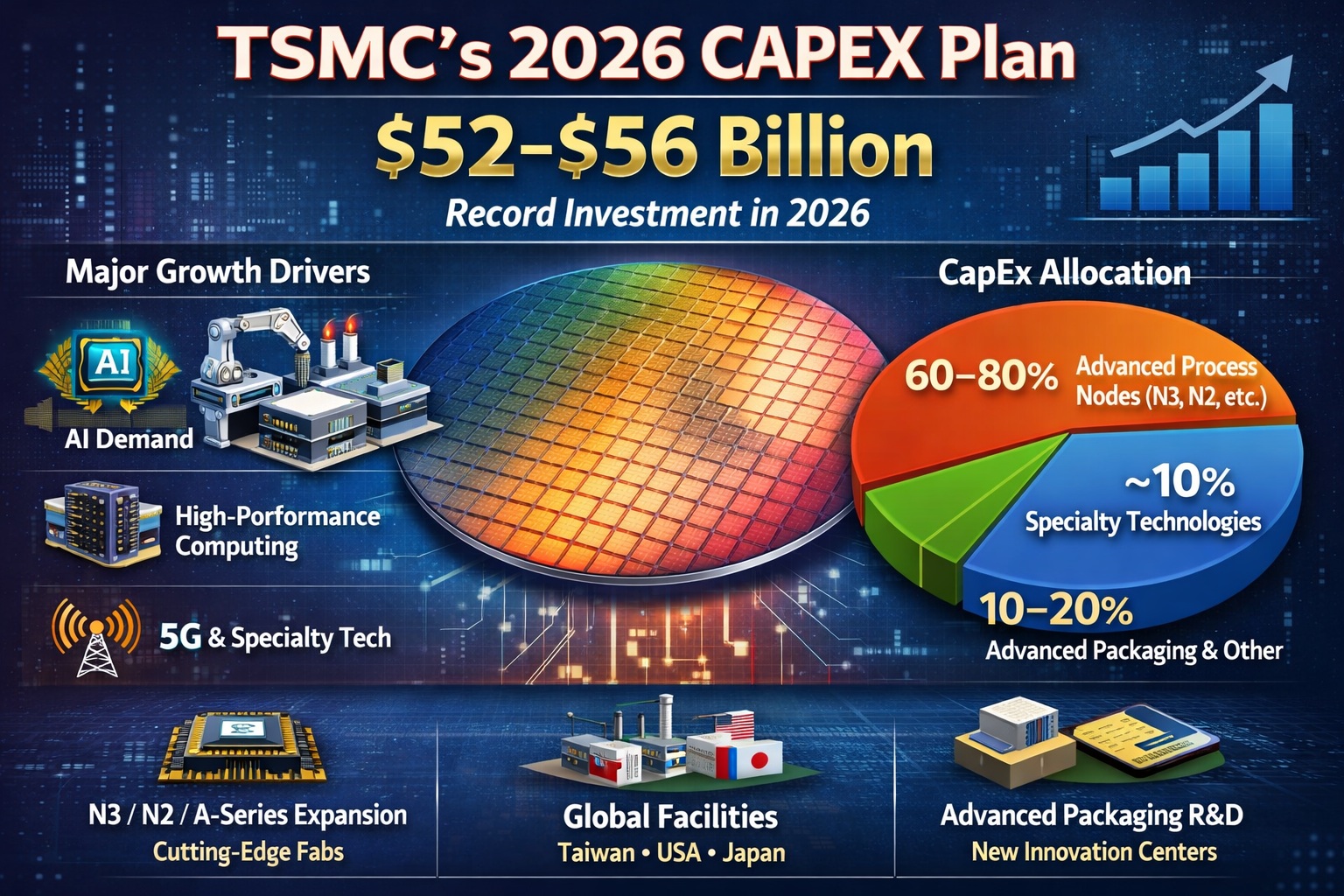

TSMC is the undisputed leader in pure-play foundry manufacturing. By focusing exclusively on manufacturing and avoiding competition with its customers in chip design, TSMC has built deep trust with fabless companies such as Nvidia, AMD, Apple, and Qualcomm. This focus has allowed TSMC to lead in process technology, consistently delivering the most advanced nodes such as N5, N3, and the upcoming N2 with strong yields and predictable execution. Its dominance has been especially visible in the AI era, where advanced nodes and packaging technologies like CoWoS have become critical bottlenecks.

Samsung Foundry represents a vertically integrated alternative. As part of Samsung Electronics, it both manufactures chips and designs its own products, including memory, logic, and consumer devices. Samsung has pushed aggressively into leading-edge nodes such as 2nm using gate-all-around (GAA) transistors and continues to invest heavily in advanced packaging and U.S. manufacturing. While Samsung has faced significant challenges in yield consistency compared to TSMC they routinely undercut TSMC wafer pricing. It is hard to figure out the math on that point. Even so, Samsung’s presence provides customers with an important second source at advanced nodes.

Intel Foundry is the most strategically significant entrant into the modern foundry race. Historically a vertically integrated company that designed and manufactured its own chips, Intel is opening its leading edge fabs to external customers while rebuilding its process leadership. Intel’s roadmap includes advanced nodes such as Intel 18A, as well as differentiated capabilities in advanced packaging (EMIB, Foveros) with U.S. based manufacturing. While Intel Foundry is still in the initial stages of winning major external customers, its success would meaningfully rebalance the industry by adding large-scale leading-edge capacity inside the United States.

Competition among these three players is not merely a commercial or political issue, it is structurally critical for the semiconductor ecosystem.

First, competition drives technological progress. Advanced chip manufacturing requires enormous capital investment, deep engineering talent, and long development cycles. Without competitive pressure, there would be less incentive to take risks on new transistor architectures, materials, or manufacturing techniques. The rapid evolution from FinFETs to GAAFET transistors is a direct result of competitive urgency.

Second, competition improves supply-chain resilience. Semiconductors are now a matter of national and economic security. Over-reliance on a single foundry or region increases vulnerability to geopolitical tensions, natural disasters, and capacity shocks. A competitive landscape with strong players in different regions reduces single-point-of-failure risk for governments and industries alike.

Third, customers benefit from choice and leverage. Fabless chip designers depend on foundries not just for wafers, but for co-optimization across design, packaging, and manufacturing. When customers have alternatives, they gain negotiating power on pricing, capacity allocation, and long-term roadmap alignment. This keeps foundries responsive to customer needs rather than dictating terms.

Finally, competition fuels ecosystem growth. Foundries anchor vast networks of equipment suppliers, materials companies, EDA vendors, and OSAT partners. When multiple foundries invest aggressively, the entire ecosystem advances faster, benefiting innovation well beyond any single company.

Bottom line: TSMC, Samsung Foundry, and Intel Foundry are not redundant competitors they are essential counterweights. The semiconductor industry needs all three to succeed, because competition ensures innovation, resilience, and sustainable growth in one of the most strategically important industries in the world, absolutely,

Also Read:

TSMC & GCU Semiconductor Training Program: Preparing Tomorrow’s Workforce

NanoIC Extends Its PDK Portfolio with First A14 Logic and eDRAM Memory PDK

TSMC’s 2026 AZ Exclusive Experience Day: Bridging Careers and Semiconductor Innovation

Share this post via:

Comments

2 Replies to “TSMC vs Intel Foundry vs Samsung Foundry 2026”

You must register or log in to view/post comments.