We are in the semiconductor market phase where everybody disagrees on what is going on. The market is up; the market is down. Mobile phones are up…. oh no, now they are down. The PC market is up—oh no, we need to wait until we can get an AI PC. The inflation is high—the consumer is not buying.

For us in the industry, the 13-week financial analyst cycle is the entire universe – time did not exist before this quarter, and it will cease to exist after it.

Sell, sell, sell, pull, push, cheat, steal, fake, blame! Anything to make the guidance number. If you are in the hamster wheel, there is no oxygen, and you lose the overview.

The bottom line is that it does not matter, and the quarterly cycles are a (sometimes expensive) distraction from achieving long-term business success. The semiconductor business does not rotate around a quarter or a financial year. It is orientated around a four-year cycle, as can be seen below.

The growth rates are high or negative – rarely moderate. The semiconductor industry is briefly in supply/demand alignment every second year. It is about as briefly aligned as two high-speed trains passing each other.

One of the primary reasons for this cyclical behaviour is the long capital investment cycle for semiconductor manufacturing. A capacity expansion might take 2-3 quarters, while a new fab takes 2-3 years to construct and fill. This leads to the first law regarding semiconductor manufacturing investments:

The first law of Semiconductor Manufacturing Investments:

“You need to invest the most when you have the least.” The quarterly hamster wheel and pressure to deliver to analysts and share squatters (There are few owners) make this law incredibly hard to follow. Failing to do so leads to the second law of semiconductor manufacturing:

The second law of Semiconductor manufacturing investments:

If you fail to abide by the first law of semiconductor manufacturing,

New capacity will come online when you need it the least.

So, a high-level and long-term strategy to create sustainable growth and profitability should be possible. That is until you learn about the third law of semiconductor manufacturing investments:

The third law of Semiconductor Manufacturing Investments:

All semiconductor cycles are different.

All semiconductor cycles are the same.

Only quantum engineers understand the third law of Semiconductor manufacturing investments. I will try and explain it anyway.

The upcycle is easy to explain. Everybody repeat after me: We are doing a great job and taking market share. Everybody is taking market share.

The down cycle is more complex. Every time I have faced a downcycle (I don’t want to reveal my age here, but is it more than a couple), I have heard new arguments about why this cycle is different: Dot Com Crash, Financial Crisis, Asia Crisis, Covid and so forth. This makes companies address this well-established cycle as something new that we might never recover from – so we have to be careful.

Once the cycle is behind us, we see it was the same as the others, plus or minus a brick.

Collectively, we never learn.

But THIS cycle is different!

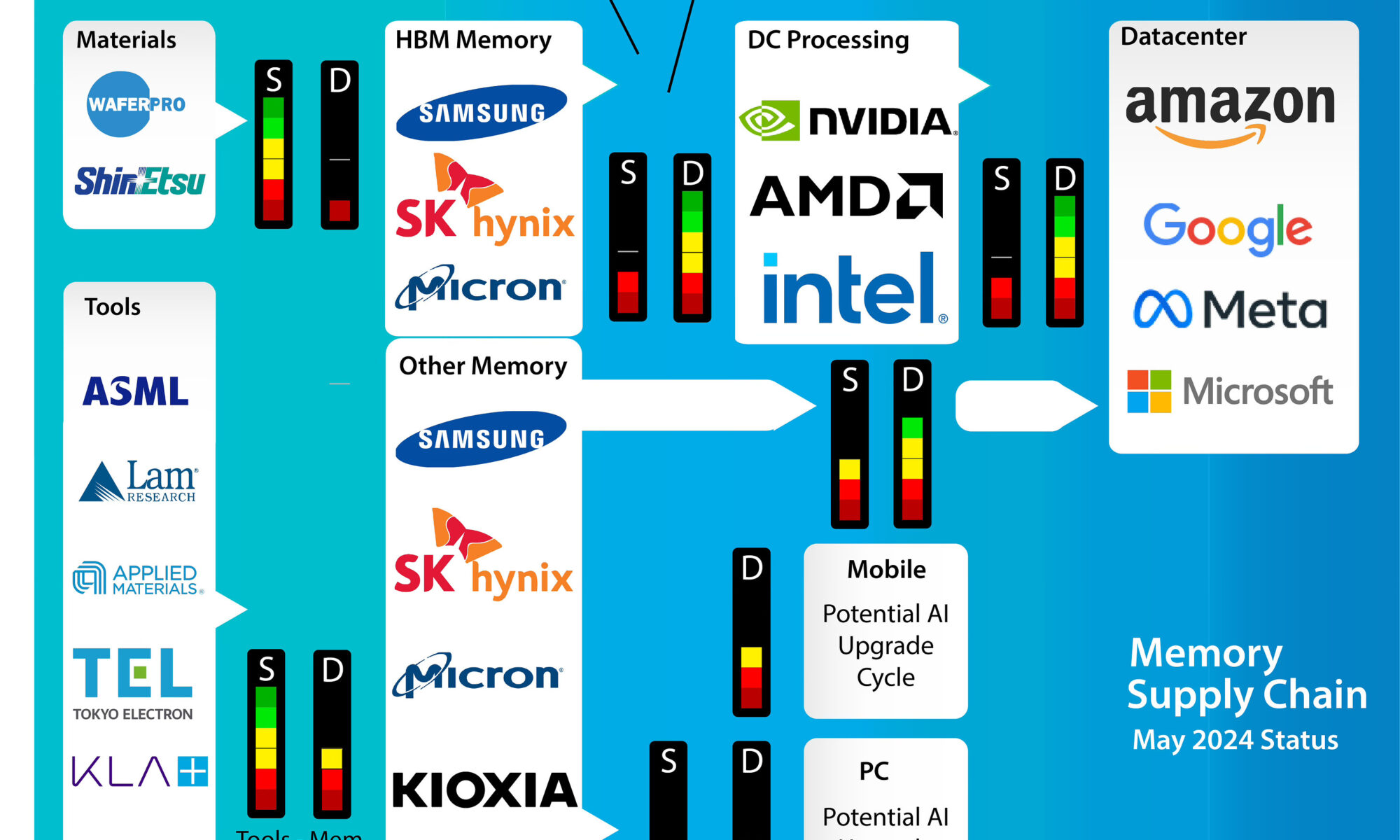

The memory markets and the three leading companies, Samsung, SK Hynix, and Micron, make the semiconductor industry even more cyclical. The market is more commodity-orientated than the rest of the industry; prices vary greatly depending on the cycle’s timing.

When the market is near a peak, memory prices are so elevated that smartphone and PC prices become prohibitive, and consumers stop buying. This propels the industry into a down-cycle.

At the bottom, where memory is sold at a loss, PCs and smartphones are so cheap that a replacement cycle initiates the next semiconductor upcycle.

Other factors impact the Semiconductor market over time (AI and GPUs are currently pushing the envelope), but the memory cycle has the most potent effect.

The combined memory revenue of the three leading companies can be seen below.

This shows the massive difference in memory companies’ profitability depending on the timing of the semiconductor cycle. In particular, the last downcycle was nasty.

This significantly impacted the memory giant’s combined capital expenditure, as seen below.

During the last down cycle, the CapEx got below the level needed to service and sustain the existing capacity (Maintenance CapEx), and there have been indications that the production capacity has declined since Q3-22.

“The best time to invest is when you have the least money.” The memory companies have failed to comply with the first law of Semiconductor Manufacturing Investment.

The lack of investment also comes at a bad time when the Memory supply chain is changing.

Large Data centre processing companies now need High Bandwidth Memory (HBM) for their AI systems. HBM needs 2x the capacity per bit than regular DRAM. As HBM is expected to be 10% of the total DRAM market in 2025, the capacity needs to increase with that amount before there is capacity for the average upcycle growth.

As the processing companies negotiate long-term contracts directly with the memory companies, they will get the capacity first. This can already be seen in general DRAM pricing, which is rising.

Two potential AI upgrade cycles for Smartphones and PCs might need extra capacity.

The Memory Capacity Outlook

As there are concerns about the large memory companies that have underinvested, it is worth taking a deeper dive into the capacity situation.

When analysing memory capacity, we investigate the historic Expansion CapEx (investment beyond maintenance) and add our projection of future expansion capex, as seen below.

Adding the Semiconductor cycles as the backdrop reveals an investment void in the 22 upcycle compared to the 18 upcycle. Companies were likely waiting with capital investments to use the Chips Act signed on August 22. Then, all memory companies were deep in the red, and only Samsung kept investing above the maintenance level to support its Taylor Fab expansion.

The Memory market has a lot of inventory, but it looks like it is drying out, revealing the severity of the capacity shortage. We will know very soon.

Samsung was the only company investing in maintenance after the Chips Act. This supported its Taylor Expansion, expected to come online in late 2024. Kudos to Samsung for timing Taylor ideally to open in the middle of the upcycle. This is the only significant capacity increase that the memory market will benefit from during this upcycle.

SK Hynix Cheongju expansion will go online precisely at the projected 26’ peak, creating the next downcycle if it is not already underway.

Micron’s Boise expansion will likely go online when the market is deep in the slide, making it difficult to make it profitable.

The semiconductor tool sales confirm that there has been no immediate response to this potential capacity shortage. An uptick in Q4-23 was not followed up in Q1-24, and the market level is generally low.

I am certainly not here to criticise the leaders of Memory companies. It is a crazy business, not for the faint of heart. When Elon Musk talked about eating glass and staring into the abyss, he was indeed speaking about the downcycle in memories.

However, if the logic in this post were applied, there might be less panic.

We have presented the facts and analysis and expect a challenging period for the memory market. However, while we trust our facts, our analysis might be misguided, and other experts can add colour to the discussion.

The Semiconductor industry is too large and complex for anybody to know it all.

Also Read:

Nvidia Sells while Intel Tells

Share this post via:

Synopsys and Intel Foundry Enable System-Level Design on Intel 14A