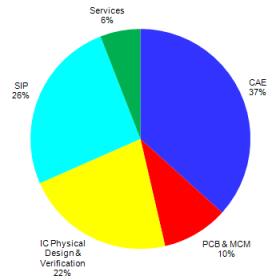

Very interesting results launched by EDAC for Q1 2011, if Computer Aided Engineering (CAE) is still the largest category with $530.6M, the second category is Silicon IP (SIP) with $371.4M, followed by IC Physical Design & Verification at $318.5M. Even more significant is the four quarter moving average results, showing growth in every category, +12.9% for CAE and +7.6% for IC PD & V, but as high as +27.9% for SIP!

To check if this really is a long term trend, I had a look at the results for Q1 2006, the same quarter five years ago. At that time, CAE results were at $510M and IC PD & V at $315M, both very close to the 2011 results and SIP was at $225M. This means that the largest two EDA categories, purely based on S/W tools, have stayed almost flat in five years, SIP has grown by 65%! If SIP keep the same growth rate (as well as CAE keep staying flat), it will take only three years for SIP to pass CAE category. In other words, we should see SIP to be the largest category as reported by EDAC during 2014.

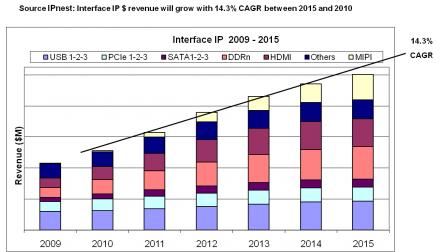

Honestly, I don’t see any reason why this would not happen. The Compound Annual Growth Rate (CAGR) for SIP (at least from the companies being part of EDAC) has been 13.5% during the last five years. The forecast we have built at IPnest for the Interface IP only exhibit a 14.3% CAGR between 2010 and 2015. In fact, if we take into account the revenues coming from ALL the IP vendors, we will see that the Silicon IP Licensing revenues are already at the same level than the CAE revenues!

From Semico: The SIP market is undergoing a round of consolidation with the number of companies shrinking approximately 50% by 2010 compared to 2000. However, this is not a sign of a weakening market, but rather of the market sorting itself out with strong contenders consolidating their positions.

Semico projects this market to continue to grow, exhibiting a CAGR of 12.6% from 2010 – 2015.

If you take a look at the EDAC member list, you will realize that, if the most important IP vendors like ARM Ltd or Synopsys are members, most of the “small” IP vendors are not. This means that the SIP category as reported by EDAC is representative of the market trends, when SIP grows, the overall IP market grows, but is not a 100% precise image of the IP market. If we consolidate the results of SIP category (from EDAC) for 2010, it comes to $1300M. We know the overall IP market is much larger, but we have no direct data. The latest available data are the 2006 results as reported by Gartner: $1 770M, including “Technology Licensing” revenue of 442.7M coming from companies like Rambus, IBM, Saifun, Nvidia or MOSAID technologies. If we decide to remove the Technology Licensing revenues, it comes to $1 327M for SIP licensing only in 2006. Then, if we apply the same growth rate that we have seen in EDAC results between 2010 and 2006, or 45%, the evaluation of the overall Silicon IP licensing revenues gives: $1 924M in 2010. This simply means that overall revenues coming from SIP category were already very close to revenues coming from CAE category in 2010! For information the later, as reported by EDAC, was at $2 006M…

By Eric Esteve from IPnest

Share this post via:

Musk’s Orbital Compute Vision: TERAFAB and the End of the Terrestrial Data Center