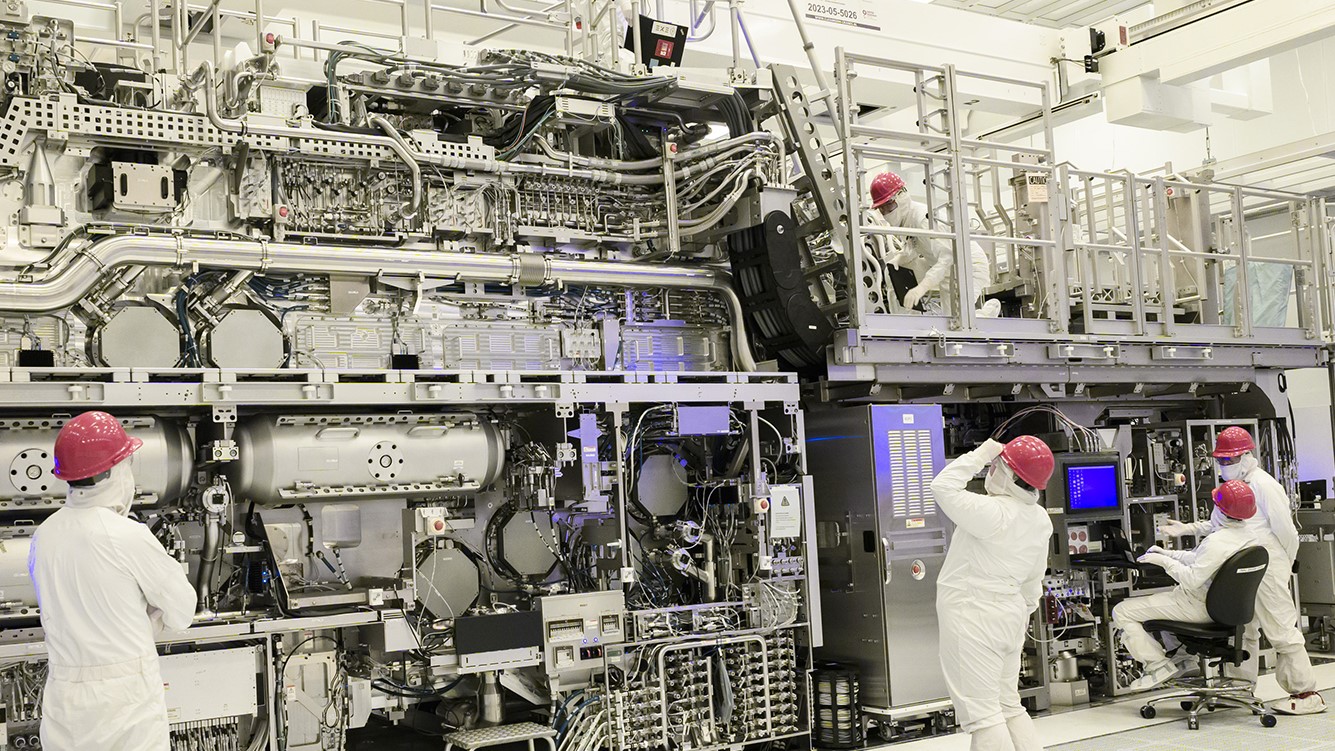

SAN FRANCISCO (Reuters) -Intel's new chief executive is exploring a big change to its contract manufacturing business to win major customers, two people familiar with the matter told Reuters, in a potentially expensive shift from his predecessor's plans.

If implemented, the new strategy for what Intel calls its "foundry" business would entail no longer marketing certain chipmaking technology, which the company had long developed, to external customers, the people said.

If implemented, the new strategy for what Intel calls its "foundry" business would entail no longer marketing certain chipmaking technology, which the company had long developed, to external customers, the people said.

") you can say the volume for those customer is low but saying no customers is kind of misleading

you can say the volume for those customer is low but saying no customers is kind of misleading