user nl

Well-known member

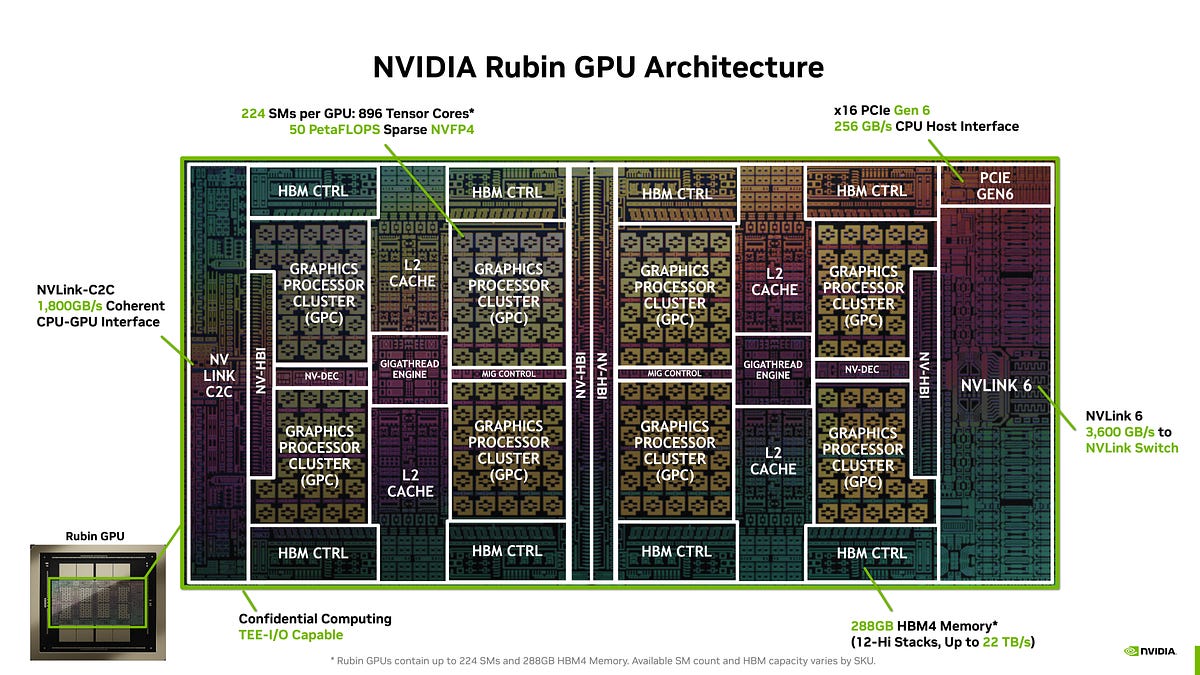

At CES 2026, Nvidia officially announced in detail all 6 Rubin platform products: the Rubin GPU, Vera CPU, NVLink 6 Switch, ConnectX-9, BlueField-4, and Spectrum-6. VR NVL72 is the second generation of Nvidia’s rack scale Oberon architecture that takes the stage. With competition catching up on rack scale game, Trainium 3 in the Gen2 UltraServer, AMD MI450X Helios Racks, and Google’s TPU which was at rack scale even before GB200, Nvidia answers with “extreme co-design” supremacy. With extreme co-design, Nvidia takes rack scale integration to the next level. Rack system becomes a unit of compute, a single distributed accelerator, and Nvidia designs the system.

newsletter.semianalysis.com

newsletter.semianalysis.com

See also:

Vera Rubin – Extreme Co-Design: An Evolution from Grace Blackwell Oberon

Vera, Rubin, NVLink 6 Switch, ConnectX-9, BlueField-4, Spectrum-6, Seamless Cableless Compute Tray Design, Power Rack, VR NVL72 TCO and BoM

newsletter.semianalysis.com

See also:

Last edited: