Disciplined execution and restored free cash flow pave the way for sustainable, profitable growth

Laurent Rémont, CEO of Soitec, commented:

“In a challenging and uncertain environment, Soitec’s FY26 performance reflects varied end-market dynamics and the Group’s deliberate actions to restore cash generation. In this context, Soitec has remained focused on disciplined execution, restoring positive Free Cash Flow and strengthening its financial position, as necessary steps toward sustainable, profitable growth. Our Q4’26 showed sequential improvement over Q3’26, above guidance, with continued momentum in AI-driven activities, in particular Photonics-SOI, a key pillar of the Group’s expansion into high-growth markets. Our priority, along with the team, is to build on these solid foundations with a clear commitment to value creation. I am confident that Soitec is well placed to thrive in a new chapter.”

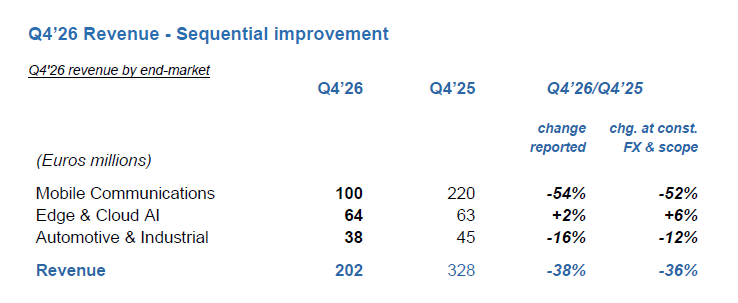

Q4’26 Revenue - Sequential improvement

Q4'26 revenue by end-market

Soitec revenue reached €202 million in Q4’26, down -38% on a reported basis and -36% at constant currency and scope, year-on-year. The decrease was primarily driven by lower volumes amid ongoing customer RF-SOI inventory correction and automotive market weakness, as well as a negative mix/price effect, partially offset by strong traction in AI markets.

Revenue improved sequentially in Q4’26, boosted by seasonal demand factors, with 25% growth vs. Q3’26 at constant currency and scope, above the initial guidance of around 20%.

Performance was mixed across end-markets. Mobile Communications continues to face RF-SOI customer inventory correction in a declining smartphone market, while subdued Automotive & Industrial revenue reflects end-market weakness. AI commercial momentum remains strong, driven by increasing Photonics-SOI penetration in high-speed pluggable transceivers and growing volumes shipped for co-packaged optics (CPOs) industry qualifications, in preparation for the upcoming ramp-up.

Mobile Communications (c. 50% of total Q4’26 revenue) - Ongoing volume impact from customer RF-SOI destocking; POI adoption gains momentum

Mobile Communications revenue came in at €100 million in Q4’26, down -52% year-on-year at constant currency and scope. A significant volume decline, reflecting customer destocking, was accompanied by a slightly positive mix effect.

RF-SOI sales declined year-on-year amid ongoing customer inventory reduction. The correction is unfolding in line with our expectations, although inventories remain high. In this context, Soitec is strengthening its technological differentiation, continuing to serve as an industry standard.

POI (Piezoelectric-on-Insulator) sales grew both year-on-year and sequentially, as Tier-1 US fabless adoption continued to offset softer demand in Asia. POI is gaining further traction in advanced SAW filters for 5G smartphones, with medium-term visibility enhanced by the long-term agreement recently signed with Skyworks, reinforcing POI’s positioning as a key substrate for next-generation architectures.

FD-SOI sales remained subdued, while showing continued progress in adoption, supported by key design wins in next-generation connectivity solutions. 5G mmWave applications continued to progress, supported by the major win secured last quarter for US flagship smartphones, and reflecting sustained customer engagement.

Edge & Cloud AI (c. 32% of total Q4’26 revenue) - Positive momentum from AI applications

Edge & Cloud AI revenue reached €64 million in Q4’26, up +6% year-on-year at constant currency and scope. This increase reflects a positive volume effect.

Photonics-SOI sales recorded strong growth year-on-year, supported by sustained investment in cloud infrastructure for AI applications. Momentum was driven by increasing adoption of silicon photonics solutions for high-speed, high-bandwidth optical transceivers.

Photonics-SOI remains a prime growth engine and a key pillar of the Group’s increasing exposure to AI-related markets. Demand is supported by structural adoption of optical interconnects in next-generation data center architectures. Soitec’s ability to deliver high-end and differentiated products to AI infrastructure value chain supports the Group’s strong position in pluggable transceivers and growing traction from co-packaged optics architectures.

FD-SOI sales were broadly stable year-on-year, with an unfavorable comparison basis, and underlying adoption momentum remains strong. FD-SOI technology remains a key enabler for AI embedded consumer, industrial, and healthcare IoT applications, offering unique advantages in power efficiency, performance, thermal management and reliability. Strong customer appetite, supported by a long-term agreement with a key customer, secures important visibility for the Group.

Automotive & Industrial (c. 19% of total Q4’26 revenue) - Customers managing inventories in soft demand environment

Automotive & Industrial revenue came to €38 million in Q4’26, down -12% year-on-year at constant currency and scope compared with Q4’25. The decline primarily reflects continued end-market weakness and customer inventory levels exceeding historical averages across the supply chain. Until we see clear signs of end market recovery and customer inventory normalization, Soitec automotive momentum should remain subdued.

Sales of Power-SOI, used in smart power management for electric vehicles, declined in Q4’26 on a year-on-year basis, reflecting continued end-market weakness and cautious ordering patterns. Delivery phasing under a long-term agreement with a key customer results in a volume and revenue concentration in Q4.

Sales of FD-SOI were broadly stable year-on-year, driven by growing volumes for Auto grade MCUs. Looking ahead, as ADAS adoption scales, the technology is proving critical for analog and mixed-signal demands of radars and microcontrollers, allowing next-generation vehicles to perceive and respond to their environment with superior power efficiency. FD-SOI is redefining automotive radar performance, enabling the fusion of precision sensing with AI processing at the edge.

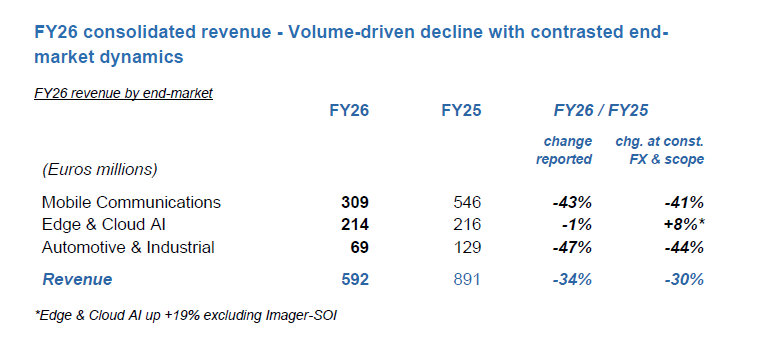

FY26 consolidated revenue - Volume-driven decline with contrasted end-market dynamics

Consolidated annual revenue came to €592 million in FY26, down -34% year-on-year as reported. This breaks down into a -30% decline at constant currency and scope, with a -1% scope effect and a -3% currency impact.

The full-year performance reflects a contraction in volumes, in an environment that remains contrasted across end-markets. Strong Edge & Cloud AI revenue growth, driven by an increasing Photonics-SOI contribution, was offset by weaker revenue from Mobile Communications and Automotive & Industrial.

Mobile Communications revenue came in at €309 million in fiscal year 2026, down -41% year-on-year at constant currency and scope. The decline was mainly driven by lower RF-SOI volumes, in line with the continued correction of customer inventory levels throughout the year.

Edge & Cloud AI revenue reached €214 million in fiscal year 2026, up +8% year-on-year at constant currency and scope. Excluding Imager-SOI, Edge & Cloud AI revenue was up +19% year-on-year at constant currency and scope. This evolution reflects positive volume and product mix dynamics, notably in photonics-related activities, as well as the contribution of FD-SOI in Edge AI applications. Strong Photonics-SOI growth momentum continues, with revenue rising above $100 million in FY26, earlier than initially anticipated, marking an important step in Soitec’s expansion into high-growth AI data center architectures.

Automotive & Industrial revenue came in at €69 million in fiscal year 2026, down -44% year-on-year at constant currency and scope. The decline was primarily driven by lower volumes in a subdued market environment, compounded by excess customer inventory.

While AI tailwinds are supporting our entire portfolio, FD-SOI and Photonics-SOI stand out as direct AI-enablers, delivering a combined year-on-year increase of +25%. These technologies directly address critical levels of the AI infrastructure: high-speed data centers and power-sensitive embedded processing, notably in IoT and wearables. This performance underscores accelerated demand in AI and the industry’s shift toward a hybrid architecture, positioning Soitec as a central enabler of seamless processing from the high-performance Cloud to the energy-efficient Edge.

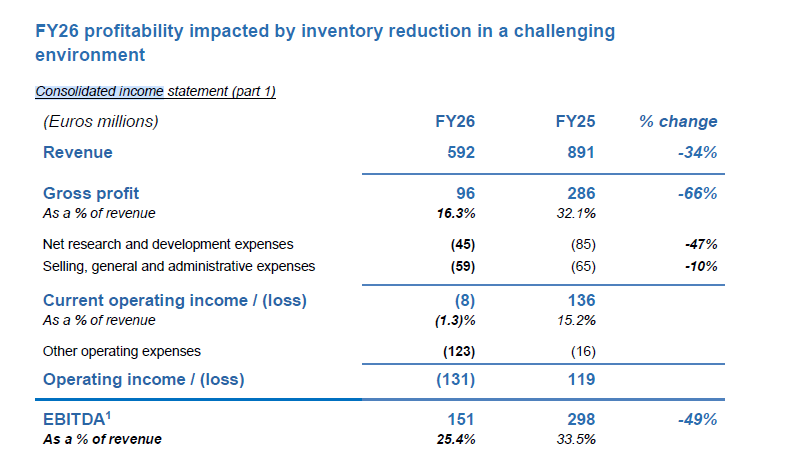

FY26 profitability impacted by inventory reduction in a challenging environment

Gross profit came in at €96 million (16.3% of revenue), down from €286 million in FY25 (32.1% of revenue). This decline primarily reflects:

● A deliberate reduction in production levels to align with our inventory-reduction objectives and end-market demand;

● an unfavorable price/mix environment;

● a negative currency impact;

● lower sales volumes, notably in RF-SOI, amid continued customer inventory correction.

These effects were partially offset by continued cost discipline and industrial efficiency measures.

Current operating result came in at a loss of €8 million in FY26, compared with a positive €136 million in FY25, mainly reflecting the decline in gross profit, partially offset by reduced operating expenses.

● Net R&D expenses decreased to €45 million (7.6% of revenue) from €85 million (9.5%). Gross R&D costs before capitalization decreased 25% to €114 million, largely resulting from reduced procurement of raw materials and the discontinuation of costs relating to Dolphin Design, divested in FY25. The Group continued to benefit from higher subsidies and research tax credits, while protecting focused innovation to support future profitable growth;

● SG&A expenses decreased to €59 million (10.0% of revenue) from €65 million (7.3%), reflecting continued strict cost discipline, including lower variable compensation and share-based payments, as well as the divestment of Dolphin Design.

Other operating expenses totaled €123 million, mainly reflecting €105 million of non-recurring impairment charges, including €41 million related to SmartSiC™ assets, €29 million on the Pasir Ris extension in Singapore, the impairment of long-term supplier advances and an earn-out loss related to the Dolphin Design disposal. As a result, Soitec recorded an operating loss of €131 million in FY26, compared with positive operating income of €119 million in FY25.

EBITDA1 declined to €151 million in FY26 from €298 million in FY25. The EBITDA margin2 decreased to 25.4% of revenue (33.5% in FY25). The margin erosion was contained by strict cost discipline and operational adjustments implemented throughout the year.

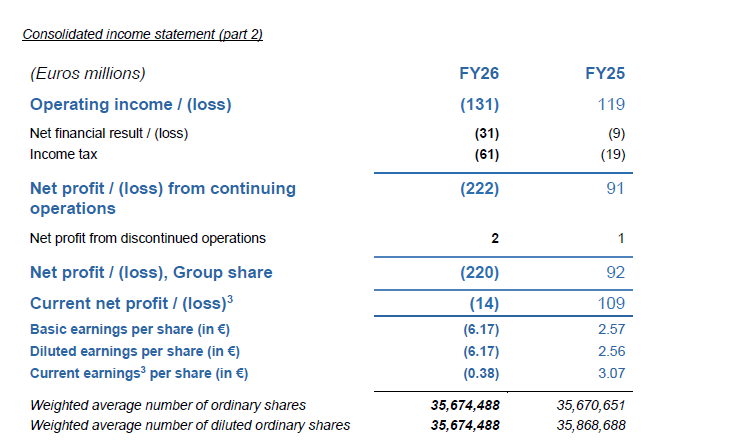

The net financial result was a loss of €31 million in FY26 (compared with a loss of €9 million in FY25), reflecting €23 million of interest expenses and a €17 million one-off foreign exchange loss recorded in Q1’26, mainly resulting from the revaluation of balance sheet foreign exchange exposure in relation to US dollar depreciation, partly offset by €13 million of financial income. Previous company policy was to protect the income statement against foreign exchange exposure; following a comprehensive review, balance sheet foreign exchange exposure is now hedged.

Income tax expense came in at €61 million in FY26, compared with €19 million in FY25, mainly reflecting the decrease in recognized deferred tax assets relating to loss carryforwards.

The current net result3 was a loss of €14 million in FY26, compared with a profit of €109 million in FY25, mainly as a result of the deterioration in operating income, non-recurring impairment charge of €105m and higher financial expenses.

The net result (Group share) was a loss of €220 million in FY26, compared with a profit of €92 million in FY25.

Positive Free Cash Flow achieved through disciplined Working Capital and Capex management

Link to Full Press Release

- - +25% sequential revenue growth in Q4’26 at constant currency and scope vs. Q3’26, exceeding the c. 20% guidance

- - €592m revenue in FY26, down -34% year-on-year on a reported basis (-30% at constant currency and scope), reflecting ongoing customer inventory correction

- - Strong momentum in Photonics-SOI, a powerful growth driver addressing surging AI data center demand, with revenue above $100m in FY26

- - FY26 EBITDA1 margin2 at 25.4% with return to positive Free Cash Flow of €63m, demonstrating disciplined execution and tight working capital management

- - Net debt / EBITDA ratio of 0.4x, underscores a robust balance sheet

- - Strategically positioned for expansion; poised to exploit growth opportunities with continued focus on execution and financial discipline

- - Q1’27 revenue expected up around 15% year-on-year, at constant currency and scope; Soitec working to reduce revenue seasonality

- - FY27 Capex cash-out expected around €100m, vs. €135m in FY26

Laurent Rémont, CEO of Soitec, commented:

“In a challenging and uncertain environment, Soitec’s FY26 performance reflects varied end-market dynamics and the Group’s deliberate actions to restore cash generation. In this context, Soitec has remained focused on disciplined execution, restoring positive Free Cash Flow and strengthening its financial position, as necessary steps toward sustainable, profitable growth. Our Q4’26 showed sequential improvement over Q3’26, above guidance, with continued momentum in AI-driven activities, in particular Photonics-SOI, a key pillar of the Group’s expansion into high-growth markets. Our priority, along with the team, is to build on these solid foundations with a clear commitment to value creation. I am confident that Soitec is well placed to thrive in a new chapter.”

Q4’26 Revenue - Sequential improvement

Q4'26 revenue by end-market

Soitec revenue reached €202 million in Q4’26, down -38% on a reported basis and -36% at constant currency and scope, year-on-year. The decrease was primarily driven by lower volumes amid ongoing customer RF-SOI inventory correction and automotive market weakness, as well as a negative mix/price effect, partially offset by strong traction in AI markets.

Revenue improved sequentially in Q4’26, boosted by seasonal demand factors, with 25% growth vs. Q3’26 at constant currency and scope, above the initial guidance of around 20%.

Performance was mixed across end-markets. Mobile Communications continues to face RF-SOI customer inventory correction in a declining smartphone market, while subdued Automotive & Industrial revenue reflects end-market weakness. AI commercial momentum remains strong, driven by increasing Photonics-SOI penetration in high-speed pluggable transceivers and growing volumes shipped for co-packaged optics (CPOs) industry qualifications, in preparation for the upcoming ramp-up.

Mobile Communications (c. 50% of total Q4’26 revenue) - Ongoing volume impact from customer RF-SOI destocking; POI adoption gains momentum

Mobile Communications revenue came in at €100 million in Q4’26, down -52% year-on-year at constant currency and scope. A significant volume decline, reflecting customer destocking, was accompanied by a slightly positive mix effect.

RF-SOI sales declined year-on-year amid ongoing customer inventory reduction. The correction is unfolding in line with our expectations, although inventories remain high. In this context, Soitec is strengthening its technological differentiation, continuing to serve as an industry standard.

POI (Piezoelectric-on-Insulator) sales grew both year-on-year and sequentially, as Tier-1 US fabless adoption continued to offset softer demand in Asia. POI is gaining further traction in advanced SAW filters for 5G smartphones, with medium-term visibility enhanced by the long-term agreement recently signed with Skyworks, reinforcing POI’s positioning as a key substrate for next-generation architectures.

FD-SOI sales remained subdued, while showing continued progress in adoption, supported by key design wins in next-generation connectivity solutions. 5G mmWave applications continued to progress, supported by the major win secured last quarter for US flagship smartphones, and reflecting sustained customer engagement.

Edge & Cloud AI (c. 32% of total Q4’26 revenue) - Positive momentum from AI applications

Edge & Cloud AI revenue reached €64 million in Q4’26, up +6% year-on-year at constant currency and scope. This increase reflects a positive volume effect.

Photonics-SOI sales recorded strong growth year-on-year, supported by sustained investment in cloud infrastructure for AI applications. Momentum was driven by increasing adoption of silicon photonics solutions for high-speed, high-bandwidth optical transceivers.

Photonics-SOI remains a prime growth engine and a key pillar of the Group’s increasing exposure to AI-related markets. Demand is supported by structural adoption of optical interconnects in next-generation data center architectures. Soitec’s ability to deliver high-end and differentiated products to AI infrastructure value chain supports the Group’s strong position in pluggable transceivers and growing traction from co-packaged optics architectures.

FD-SOI sales were broadly stable year-on-year, with an unfavorable comparison basis, and underlying adoption momentum remains strong. FD-SOI technology remains a key enabler for AI embedded consumer, industrial, and healthcare IoT applications, offering unique advantages in power efficiency, performance, thermal management and reliability. Strong customer appetite, supported by a long-term agreement with a key customer, secures important visibility for the Group.

Automotive & Industrial (c. 19% of total Q4’26 revenue) - Customers managing inventories in soft demand environment

Automotive & Industrial revenue came to €38 million in Q4’26, down -12% year-on-year at constant currency and scope compared with Q4’25. The decline primarily reflects continued end-market weakness and customer inventory levels exceeding historical averages across the supply chain. Until we see clear signs of end market recovery and customer inventory normalization, Soitec automotive momentum should remain subdued.

Sales of Power-SOI, used in smart power management for electric vehicles, declined in Q4’26 on a year-on-year basis, reflecting continued end-market weakness and cautious ordering patterns. Delivery phasing under a long-term agreement with a key customer results in a volume and revenue concentration in Q4.

Sales of FD-SOI were broadly stable year-on-year, driven by growing volumes for Auto grade MCUs. Looking ahead, as ADAS adoption scales, the technology is proving critical for analog and mixed-signal demands of radars and microcontrollers, allowing next-generation vehicles to perceive and respond to their environment with superior power efficiency. FD-SOI is redefining automotive radar performance, enabling the fusion of precision sensing with AI processing at the edge.

FY26 consolidated revenue - Volume-driven decline with contrasted end-market dynamics

Consolidated annual revenue came to €592 million in FY26, down -34% year-on-year as reported. This breaks down into a -30% decline at constant currency and scope, with a -1% scope effect and a -3% currency impact.

The full-year performance reflects a contraction in volumes, in an environment that remains contrasted across end-markets. Strong Edge & Cloud AI revenue growth, driven by an increasing Photonics-SOI contribution, was offset by weaker revenue from Mobile Communications and Automotive & Industrial.

Mobile Communications revenue came in at €309 million in fiscal year 2026, down -41% year-on-year at constant currency and scope. The decline was mainly driven by lower RF-SOI volumes, in line with the continued correction of customer inventory levels throughout the year.

Edge & Cloud AI revenue reached €214 million in fiscal year 2026, up +8% year-on-year at constant currency and scope. Excluding Imager-SOI, Edge & Cloud AI revenue was up +19% year-on-year at constant currency and scope. This evolution reflects positive volume and product mix dynamics, notably in photonics-related activities, as well as the contribution of FD-SOI in Edge AI applications. Strong Photonics-SOI growth momentum continues, with revenue rising above $100 million in FY26, earlier than initially anticipated, marking an important step in Soitec’s expansion into high-growth AI data center architectures.

Automotive & Industrial revenue came in at €69 million in fiscal year 2026, down -44% year-on-year at constant currency and scope. The decline was primarily driven by lower volumes in a subdued market environment, compounded by excess customer inventory.

While AI tailwinds are supporting our entire portfolio, FD-SOI and Photonics-SOI stand out as direct AI-enablers, delivering a combined year-on-year increase of +25%. These technologies directly address critical levels of the AI infrastructure: high-speed data centers and power-sensitive embedded processing, notably in IoT and wearables. This performance underscores accelerated demand in AI and the industry’s shift toward a hybrid architecture, positioning Soitec as a central enabler of seamless processing from the high-performance Cloud to the energy-efficient Edge.

FY26 profitability impacted by inventory reduction in a challenging environment

Gross profit came in at €96 million (16.3% of revenue), down from €286 million in FY25 (32.1% of revenue). This decline primarily reflects:

● A deliberate reduction in production levels to align with our inventory-reduction objectives and end-market demand;

● an unfavorable price/mix environment;

● a negative currency impact;

● lower sales volumes, notably in RF-SOI, amid continued customer inventory correction.

These effects were partially offset by continued cost discipline and industrial efficiency measures.

Current operating result came in at a loss of €8 million in FY26, compared with a positive €136 million in FY25, mainly reflecting the decline in gross profit, partially offset by reduced operating expenses.

● Net R&D expenses decreased to €45 million (7.6% of revenue) from €85 million (9.5%). Gross R&D costs before capitalization decreased 25% to €114 million, largely resulting from reduced procurement of raw materials and the discontinuation of costs relating to Dolphin Design, divested in FY25. The Group continued to benefit from higher subsidies and research tax credits, while protecting focused innovation to support future profitable growth;

● SG&A expenses decreased to €59 million (10.0% of revenue) from €65 million (7.3%), reflecting continued strict cost discipline, including lower variable compensation and share-based payments, as well as the divestment of Dolphin Design.

Other operating expenses totaled €123 million, mainly reflecting €105 million of non-recurring impairment charges, including €41 million related to SmartSiC™ assets, €29 million on the Pasir Ris extension in Singapore, the impairment of long-term supplier advances and an earn-out loss related to the Dolphin Design disposal. As a result, Soitec recorded an operating loss of €131 million in FY26, compared with positive operating income of €119 million in FY25.

EBITDA1 declined to €151 million in FY26 from €298 million in FY25. The EBITDA margin2 decreased to 25.4% of revenue (33.5% in FY25). The margin erosion was contained by strict cost discipline and operational adjustments implemented throughout the year.

The net financial result was a loss of €31 million in FY26 (compared with a loss of €9 million in FY25), reflecting €23 million of interest expenses and a €17 million one-off foreign exchange loss recorded in Q1’26, mainly resulting from the revaluation of balance sheet foreign exchange exposure in relation to US dollar depreciation, partly offset by €13 million of financial income. Previous company policy was to protect the income statement against foreign exchange exposure; following a comprehensive review, balance sheet foreign exchange exposure is now hedged.

Income tax expense came in at €61 million in FY26, compared with €19 million in FY25, mainly reflecting the decrease in recognized deferred tax assets relating to loss carryforwards.

The current net result3 was a loss of €14 million in FY26, compared with a profit of €109 million in FY25, mainly as a result of the deterioration in operating income, non-recurring impairment charge of €105m and higher financial expenses.

The net result (Group share) was a loss of €220 million in FY26, compared with a profit of €92 million in FY25.

Positive Free Cash Flow achieved through disciplined Working Capital and Capex management

Link to Full Press Release