Xebec

Well-known member

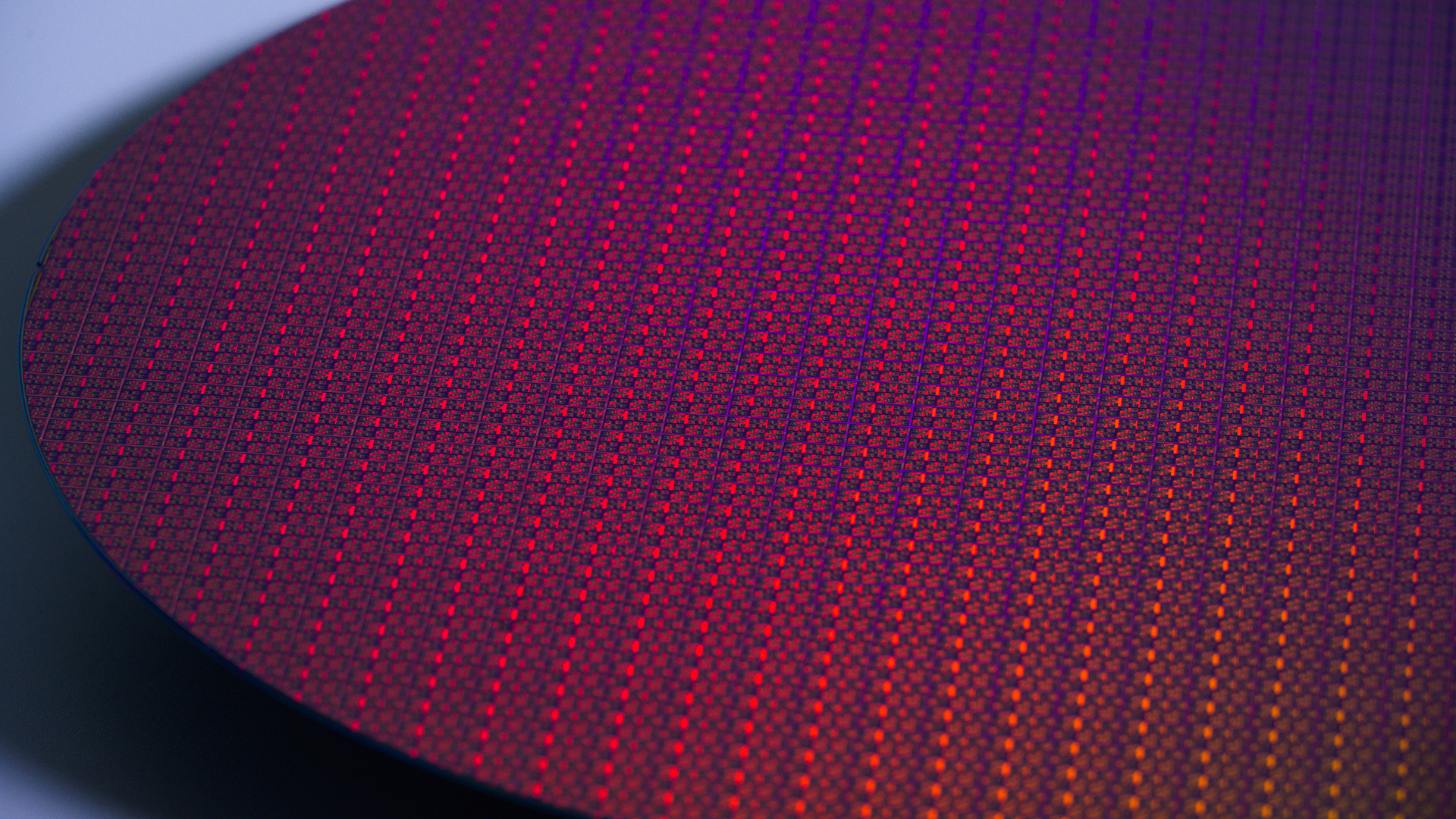

Continued Momentum for Intel 18A

Progress on lead product designs and process readiness is enabling us to bridge from Intel 20A earlier than we’d planned.

www.intel.com

www.intel.com

One of the benefits of our early success on Intel 18A is that it enables us to shift engineering resources from Intel 20A earlier than expected as we near completion of our five-nodes-in-four-years plan. With this decision, the Arrow Lake processor family will be built primarily using external partners and packaged by Intel Foundry.

(I was personally really hoping to see proof of yield with Arrow Lake 20A…)

")