Global Semiconductor Market Outlook: 2025 to 2034

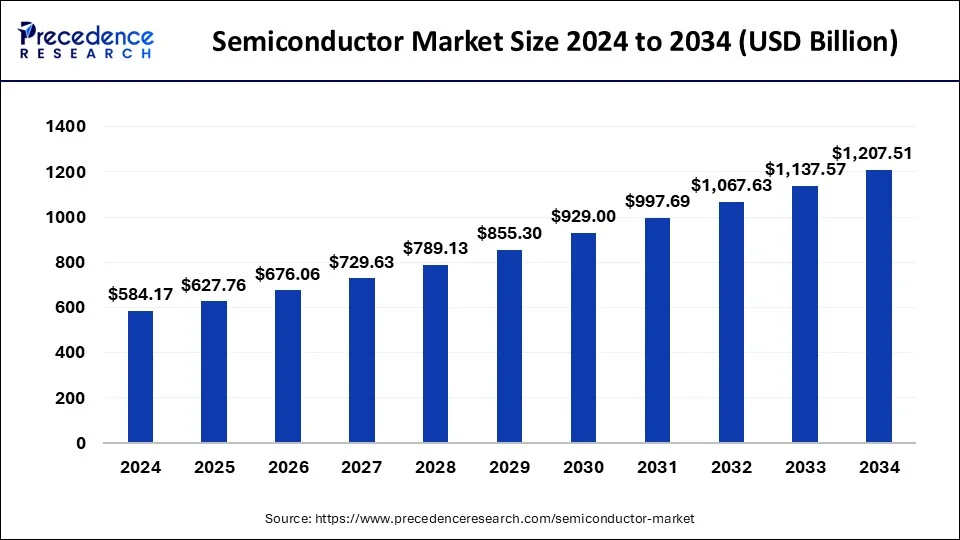

The global semiconductor market is entering a transformative era, projected to grow from USD 627.76 billion in 2025 to USD 1,207.51 billion by 2034, at a compound annual growth rate (CAGR) of 7.54%. This robust growth reflects rising global demand for connected devices, artificial intelligence (AI), 5G, edge computing, and electric vehicles (EVs), all of which are heavily reliant on semiconductor technologies.

After a downturn in 2023—marked as the industry’s seventh decline since 1990—global semiconductor sales fell by 9.4% to USD 520 billion. However, thanks to a stronger-than-expected recovery in Q2 and Q3, 2024 is forecasted to see a sharp rebound, with projected revenues of USD 588 billion, surpassing the record-breaking 2022 sales. The industry’s resilience is attributed to demand from AI, cloud computing, and a shift to advanced chiplet-based system architectures.

Asia Pacific remains the largest and most dominant regional market, with a 2024 market share of 52.93%, driven by countries like China, Taiwan, and South Korea. These nations benefit from strong electronics manufacturing ecosystems, rising consumer demand, and accelerating adoption of IoT, AI, and smart devices. The region’s market is projected to more than double, reaching USD 650.02 billion by 2034. Meanwhile, North America and Europe are anticipated to experience the fastest growth, supported by government investment, advanced telecom infrastructure, and robust automotive sectors.

By component, memory devices led in 2024, spurred by cloud storage, HBM for AI, and increasing memory density in consumer electronics. Other notable components include microprocessors (MPUs), microcontrollers (MCUs), logic devices, and analog ICs. The networking and communications segment dominated in terms of application share (29.75%), owing to the proliferation of smartphones, 5G rollouts, and high-speed internet demand. The automotive segment is poised for rapid growth due to the electrification trend, rising demand for autonomous and connected vehicles, and adoption of Advanced Driver Assistance Systems (ADAS).

Global governments are actively supporting semiconductor development. The U.S. CHIPS Act earmarks $52 billion for domestic manufacturing and R&D. India’s Semicon program allocates INR 76,000 crore to boost chip production, while Canada is investing over USD 180 million in local fabrication capacity. These strategic initiatives aim to strengthen domestic supply chains, promote innovation, and ensure geopolitical competitiveness.

Despite the growth prospects, the industry faces significant challenges: elevated inventory levels exceeding $60 billion, declining fab utilization rates (expected to fall below 70% by end-2023), and continued supply chain vulnerabilities. A shortage of skilled labor and high production complexity add to operational headwinds. Additionally, a shortage of silicon wafers may limit supply in the near term.

Looking ahead, market opportunities include increasing semiconductor content in EVs, rising demand for autonomous vehicles, and adoption of advanced packaging (e.g., 3D ICs, Fan-Out, SiPs). Memory advancements such as 3D NAND and next-gen DRAM are reshaping data center infrastructure.

Bottom line: The global semiconductor market is poised for sustained expansion, underpinned by macroeconomic trends, government support, and technological evolution. Companies that embrace AI, chiplet design, and supply chain innovation will be best positioned to lead this new era of semiconductor-driven growth.

Semiconductor Market Size to Hit Around USD 1,207.51 Billion by 2034

The global semiconductor market size was calculated at USD 584.17 billion in 2024 and is projected to hit around USD 1,207.51 billion by 2034, growing at a CAGR of 7.54%