I hope they can hold market share after next gen EPYC releases. Do you think that's plausible given intel 3 server chips will release around 6 months later?

The question becomes, does Intel's competitive situation get worse, better, or roughly the same, I think.

Sapphire Rapids is good at single-threaded, and also scales beyond two processors. It also has custom chiplets that make the processor especially good at specific tasks. However, even now, in 2P stations, they trail behind AMD is most workloads. On the other hand, very few processors are sold with the highest chip counts.

I'd say, they can probably hold onto share, because Emerald Rapids is coming out, and I don't think the situation will get much worse. I also don't think Emerald Rapids will significantly alter their situation, as it's a relatively minor bump, and not as broad a product release as Sapphire Rapids was (for example, it's limited to 2P I believe).

Sierra Forest will help some, but I don't think it's a great product. But, it's a far better approach than AMD's, with their Zen 4C. I guess AMD didn't want to invest the money in a more power efficient architecture and felt tweaking Zen 4 was good enough. It's not without advantages, but overall, I think it's a poor approach vis-a-vis designing a processor from the ground up for specific characteristics.

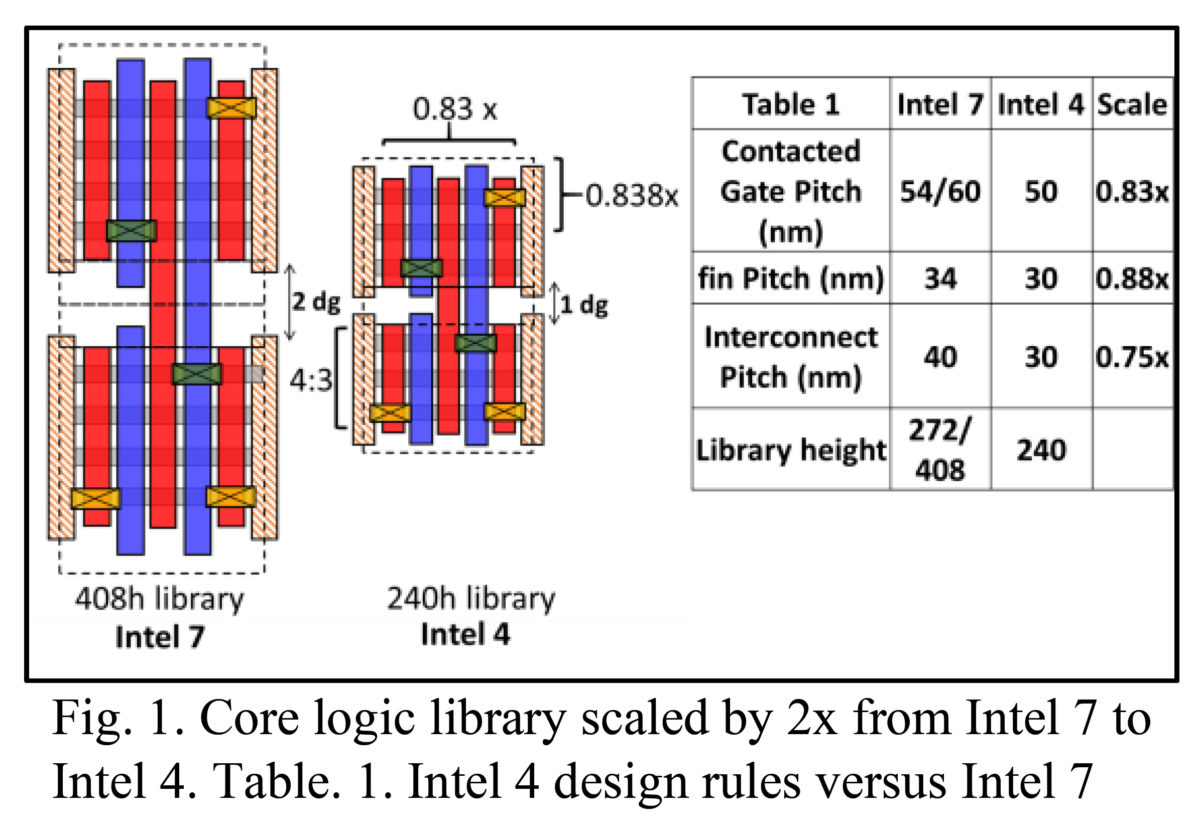

But, TSMC is so far ahead, if we compare Intel 7 with 5nm, in low power efficiency, it still is competitive for AMD. It won't necessarily always be.

By the looks of things, Intel 3 is a weak release, basing this not only on information provided here, but also on the almost complete lack of interest in it by third parties. Some of that is timing, of course, and other factors, but I also think it's not a particularly compelling process when compared to TSMC's leading nodes. But, is it closer to TSMC 3nm than Intel 7 is to TSMC 5nm, which is the current situation?

Of course, Intel 7 is considerably better than TSMC 5nm in clock speed, but I mean for server applications, and it's not even close there. Not in power efficiency, and not in density. And yes, we don't have the same chip designed on both processes, and there's always a degree of uncertainty, but if we're being real, this is how things are.

So, I think Intel will close the gap with Intel 3, but I don't think it's going to be as a good a process for server chips, overall, as TSMC 3nm. So, I think they can hold market share, since the competitive landscape should switch more in their favor, but I still don't think Granite Rapids is going to gain share the way they say it will, or at least alluded to. And I think Sierra Forest is the start of something big, but I don't see it gaining significant traction in its first iteration.

Based on information provided here, and by Intel (that they are way ahead on PowerVia technology), and the much more common references to external partner interest in Intel 18A, I think Intel may have an opportunity there to regain market share in servers. Before then, I just don't think it's an easy argument to make. Equally, I don't think AMD's competitive situation, which I view as already quite strong, will increase significantly going forward.

Of course, I really have no idea, these are just opinions from the cheap seats.

I do think they'll keep doing well, possibly even better, in client though. Everything points to it.

But, what I find a bit disturbing is, Intel doesn't seem to be making a client part on Intel 3. Just server parts. Given the data provided earlier here, and remarks by Daniel regarding expected power efficiency, it doesn't seem to be an ideal part for servers, but would be quite good in client. And given it seems to have limited interest from outside companies, Intel 3 is something of a mystery to me. It will be largely by server parts, which it isn't ideal for? Something isn't adding up, but I guess we'll find out what's missing as time goes on.