You are currently viewing SemiWiki as a guest which gives you limited access to the site. To view blog comments and experience other SemiWiki features you must be a registered member. Registration is fast, simple, and absolutely free so please, join our community today!

I remembered TSMC's CFO was asked by an analyst about such type of financing deals during their Q3 2022 earnings conference call. His answer was: it's too expensive.

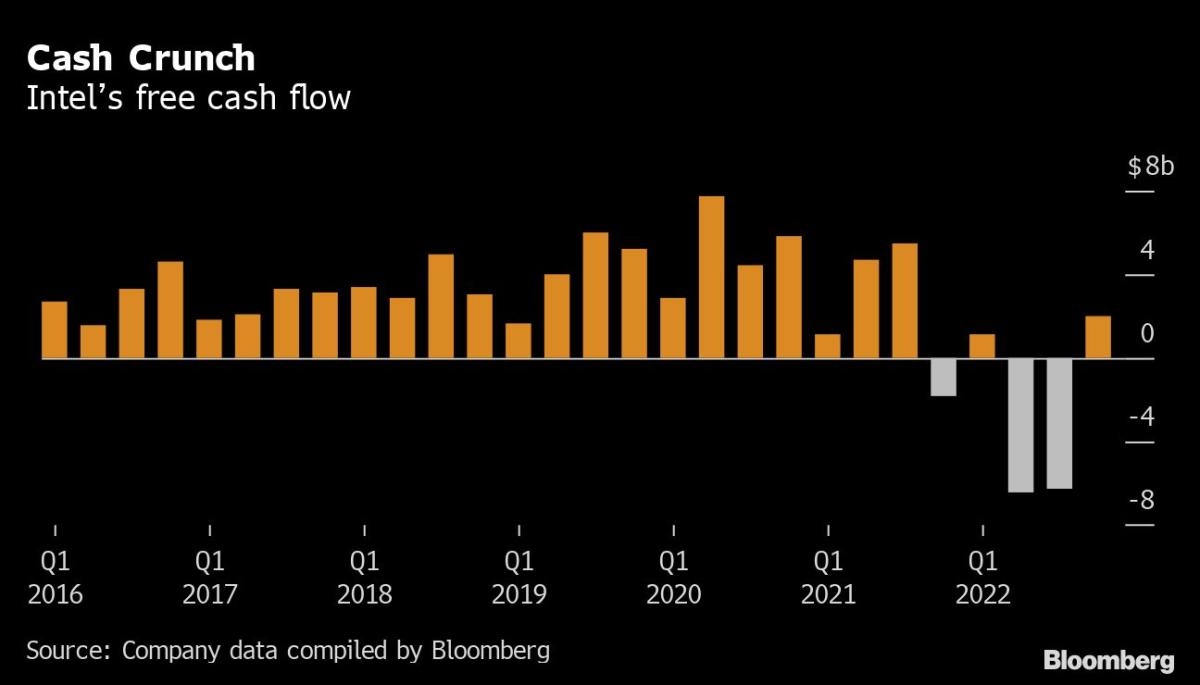

(Bloomberg Markets) -- Brookfield Infrastructure Partners LP’s $15 billion commitment last year to help finance Intel Corp.’s giant new semiconductor complex in Arizona, the first deal of its kind, sent investors and bankers racing to find similar opportunities.Most Read from BloombergMerck...

I remembered TSMC's CFO was asked by analyst about such type of financing deals during their Q3 2022 earnings conference call. His answer was: it's too expensive.

(Bloomberg Markets) -- Brookfield Infrastructure Partners LP’s $15 billion commitment last year to help finance Intel Corp.’s giant new semiconductor complex in Arizona, the first deal of its kind, sent investors and bankers racing to find similar opportunities.Most Read from BloombergMerck...

While not too much new was in here it was an interesting read; thanks for sharing.

As for this being too expensive for TSMC I agree it is not the play for them. But that isn’t surprising since they have plenty of cash in the bank and much better access to low interest debt. I don’t know if that proposal on tax credits for equipment spend passed in the ROC, but if it did that will certainly be better than what intel or TSMC would be getting from CHIPS.

I’d love to get more specifics on this deal, but based on what we know it seems like the right play for intel to grow their capacity sufficiently to even have a chance of becoming a relevant foundry player.

I would imagine the Brookfield maneuver enables Intel debt to remain investment grade. That is worth more to Intel than TSMC, which is highly credit worthy by comparison.

I would also imagine Brookfield will suck up every dollar of Intel free cash flow, excluding the dividend, most quarters, once the disbursements start. So it's burdensome. There will be no escaping a massive culture change at Intel, from spendthrift to thrifty. That may be part of the intention, too.

I would imagine the Brookfield maneuver enables Intel debt to remain investment grade. That is worth more to Intel than TSMC, which is highly credit worthy by comparison.

I would also imagine Brookfield will suck up every dollar of Intel free cash flow, excluding the dividend, most quarters, once the disbursements start. So it's burdensome. There will be no escaping a massive culture change at Intel, from spendthrift to thrifty. That may be part of the intention, too.

Really seems like mortgaging the future from my perspective. Brookfield is a pure asset manager. They are experts at squeezing every last dollar out of an investment. I’m curious how this will pan out.

1. In a few years those specialized fab equipment can lose its value quickly or become much less competitive due to technology advancement. As a shareholder Brookfield can't just shut the door and walk away. The risks Brookfield exposed to is huge. They must have received generous return and downside protection.

2. In order to generate enough profit to pay for the promised return to Brookfield, Intel must have guaranteed this new Arizona fab that Brookfield-Intel venture owned will constantly have high utilization rate. Does that mean some other Intel fabs will be forced to lose their volume to this new cousin? Does this new cousin's interest always align with the Intel's?

3. Because Brookfield got guaranteed minimum return, I believe they also certainly got a preferred exit clause based on time/years or Intel's performance. That won't be cheap for Intel.

1. In a few years those specialized fab equipment can lose its value quickly or become much less competitive due to technology advancement. As a shareholder Brookfield can't just shut the door and walk away. The risks Brookfield exposed to is huge. They must have received generous return and downside protection.

2. In order to generate enough profit to pay for the promised return to Brookfield, Intel must have guaranteed this new Arizona fab that Brookfield-Intel venture owned will constantly have high utilization rate. Does that mean some other Intel fabs will be forced to lose their volume to this new cousin? Does this new cousin's interest always align with the Intel's?

3. Because Brookfield got guaranteed minimum return, I believe they also certainly got a preferred exit clause based on time/years or Intel's performance. That won't be cheap for Intel.

finance.yahoo.com

finance.yahoo.com