Intel (INTC) shares have surged 3x year-to-date due to increasing CPU demand and heightened optimism regarding its foundry operations. Investors are starting to recognize Intel Corporation as more than just a cyclical PC manufacturer. The market is beginning to factor in the likelihood that Intel could become a significant alternative source for cutting-edge semiconductor production, alongside Taiwan Semiconductor Manufacturing Company.

A portion of this optimism is driven by geopolitical factors.

Both governments and hyperscalers are keen on establishing more advanced chip fabrication within the United States, especially for AI infrastructure and military-related computing. Intel’s manufacturing presence positions it centrally within that transition.

However, being situated in the U.S. has its limitations.

The critical factor is whether Intel can compete effectively on technology, yields, manufacturing scale, and production economics. More crucially, can Intel establish itself as a foundry that major external clients can depend on consistently for leading-edge nodes?

A rule-based investing strategy provides the objective framework necessary to navigate volatile turnaround stories like Intel, safeguarding portfolios against steep foundry execution and yield risks through systematic, data-driven asset allocation.

Intel Has Closed The Technology Gap

Intel’s 18A process signifies the company's most significant manufacturing advancement in years, which is a major factor in the increasingly positive perceptions toward the foundry business. Throughout much of the last decade, Intel was seen as structurally trailing TSMC in advanced chip manufacturing.

This gap has now narrowed considerably.

Intel’s latest manufacturing technology aims to enhance chip performance while reducing power consumption—two critical metrics in AI infrastructure and advanced computing systems where energy and cooling expenses are becoming significant constraints.

While TSMC still has a lead in manufacturing efficiency and transistor density, enabling clients to create smaller and more energy-efficient chips, Intel’s forthcoming 14A process is anticipated to adopt next-generation High-NA EUV lithography prior to TSMC’s equivalent future nodes. If executed properly, this could provide Intel with a temporary technological edge at the forefront, despite substantial execution risks.

Scale And Customer Confidence Still Favor TSMC

The financial and operational disparity between the two foundries is still vast.

TSMC reported $35.9 billion in foundry revenue in the first quarter of 2026, juxtaposed with Intel Foundry’s $5.4 billion. Nearly all of TSMC’s revenue was sourced from external clients, while Intel Foundry earned only about $174 million from outside customers, accounting for roughly 3% of total foundry revenue. The remainder primarily reflects Intel manufacturing chips for its internal product divisions.

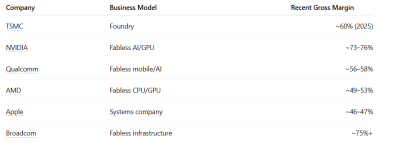

This distinction is crucial because foundry economics benefit from scale, utilization, and customer diversity. TSMC’s operating margin reached 58.1% in the quarter, bolstered by a high demand for advanced AI and high-performance computing chips. Technologies at 7nm and below represented approximately 74% of TSMC’s wafer revenue, with 3nm alone contributing 25%.

Scale also reinforces TSMC’s manufacturing ecosystem. The company operates at a significantly larger scale, with capacities covering manufacturing, packaging, IP libraries, and customer integration developed over decades. Its execution track record and mature yields have established it as the industry’s default manufacturing partner for Apple (AAPL), Nvidia (NVDA), AMD (AMD), and Qualcomm (QCOM).

Intel is operating in a very different phase of its cycle. The company is still managing substantial fab construction and tooling expenses while increasing advanced-node production. The foundry division recorded a loss exceeding $10 billion in the last quarter. In comparison, Intel Foundry remains considerably smaller, even with significant investments in Arizona and other U.S. facilities.

Yield Is The Crucial Test

Leadership in technology alone does not dictate foundry success. Yield and execution are more critical.

Yield measures the percentage of chips on a wafer that operate correctly after manufacturing. At advanced nodes, wafers can surpass $30,000 before the packaging and testing phases, indicating that even slight yield variations can significantly influence profitability.

Intel’s 18 A yield reportedly rose from around 50% to 55% by mid-2025, with internal aspirations of reaching 65% to 70% by year-end. TSMC’s N2 yields were estimated at approximately 65% and climbed to around 70% by early 2026, with anticipated maturity yields of about 75%.

This 10 to 15% point difference is commercially important because higher yields reduce the cost per usable chip. For clients, improved yields can also mitigate production risks and enhance the reliability of scaling large AI deployments on schedule.

The Bottom Line

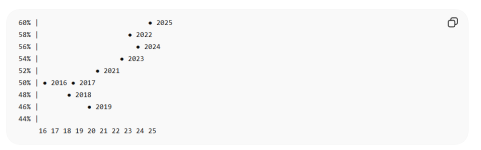

Business expectations remain exceptionally high. Intel’s price-to-sales ratio has soared from roughly 1.6x a year ago to almost 10x currently, reflecting increasing investor assurance that the company can serve as a credible second source for advanced semiconductor manufacturing in the United States. However, maintaining this optimism will necessitate more than a restored technology strategy. (See how Intel’s margins compare with peers) Intel must now demonstrate its capacity to manufacture advanced chips at scale, with competitive yields, trustworthy execution, and the consistency that major customers expect from a premier foundry.

Why Intel Still Trails TSMC In The High Stakes Foundry Race

Both governments and hyperscalers are keen on establishing more advanced chip fabrication within the United States, especially for AI infrastructure and...

www.forbes.com

www.forbes.com

) but from what I have been told the Samsung 1.4 process has been delayed due to 2nm yield learning.

) but from what I have been told the Samsung 1.4 process has been delayed due to 2nm yield learning.